Deep Dives with Real Vision's Chief Crypto Analyst, Jamie Coutts.

September 13, 2024

The past six months have been tough for crypto markets, but a strong foundation is being laid beneath the surface of volatile prices and supply overhangs. Smart contract platforms (SCP) — the backbone of the digital asset ecosystem — are quietly experiencing increased adoption and capital inflows. Despite concerns over potential political headwinds — a Harris victory or a more fiscally responsible Republican government could impact sentiment — the basis for assessing a secular technology, Blockchain, or adoption, appears to have its own momentum at this point.

The key questions remain: Is the crypto economy growing? By how much? And by what measures should we define it? The answers to these questions will be our guiding light and should shape decisions about exposure to digital assets.

This report offers an update on the state of crypto markets, with a particular focus on the SCP sector. It also includes the beta versions of the SCP Network and Asset Pulse dashboards, which — though delayed — are set to form the core of the Real Vision Pro Crypto dashboards.

Key Takeaways

- Nearing Market Bottom: The severe correction is exhibiting signs of exhaustion, with most metrics at extremes and fewer assets hitting new lows. Bitcoin’s strong Q4 seasonality could signal a market reversal.

- Bullish Liquidity Setup: Dollar weakness and central bank balance sheet injections are driving a bullish liquidity environment, with the MSI flashing its first bullish signal since November 2023 in August.

- Robust Network Growth: Active addresses have surged during the correction and TVL remains resilient, showing strong capital inflows despite weak price action.

- Fee Decline Explained: EIP-4844 and crypto’s reflexive price dynamics crush fee revenue for L1s.

- Ethereum Dominance: Relative to the SCP sector, ETH is at a critical inflection point —poised for a breakdown or a strong recovery.

Crypto Market Update

The mid-cycle bear market, which kicked off in March/April, has continued its downward grind since our last update in early August.

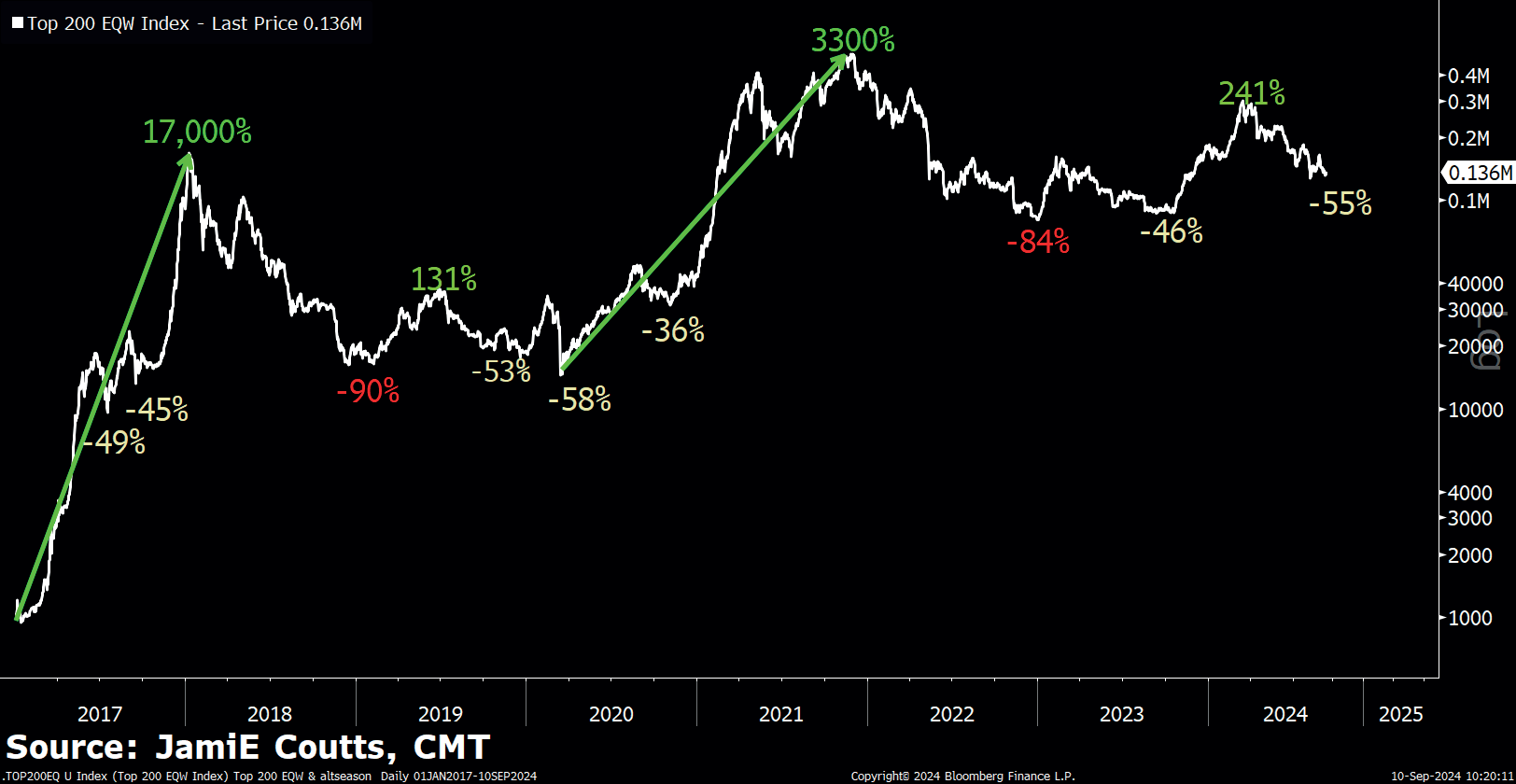

While it’s uncomfortable, a 55% pullback from the Q1 peak in the equal-weighted Top 200 index isn’t out of the ordinary. In previous cycles, once the market bottomed in 2018 and 2022, we saw multiple 40-60% corrections. The chart below captures the rollercoaster ride of investing in this asset class — it’s never a smooth path.

Market Breadth

A quick glance at the equal-weight index chart reveals that market breadth is still in the gutter. Naturally, large-cap names like Bitcoin (down 21%), Ethereum (down 41%), and Solana (down 35%) have performed better than the average altcoin. This has helped the market cap-weighted Top 200 stay positive YTD (+14.69%), outperforming the equal-weighted Top 200, which is down 22.43% due to its heavier skew toward alts and small caps.

The Altseason indicator, which tracks how many of the Top 200 assets have outperformed Bitcoin over the last 90 days, has been stuck between 10-15% for the past 3 months. Historically, this indicator bottoms out at 6-9% during extreme bearish phases. Although we can’t rule out another downdraft, I suspect the market is closer to the final stages of this sentiment washout.

As covered in previous reports, alts likely won’t find their footing until Bitcoin decisively clears its all-time high, which we will see in the next section will be driven by increasing central banks easing liquidity in Q4.

To avoid redundancy, I’ll just say this: all other breadth measures in my toolkit paint an equally if not more, bearish picture of market positioning. From a breadth perspective, it is as bearish today as it was in mid-2022 when the market was rapidly approaching the capitulation lows.

Below are three key breadth indicators, each telling a different part of the same story:

- Advance/Decline Line (ADL): The ADL, which tracks the net daily advances across the Top 40 assets, remains in a solid downtrend. However, the ADL momentum oscillator is forming a bullish divergence (higher low), hinting that this downward move may be nearing exhaustion.

- Top 20 Assets Above their 200-Day Moving Average: Only 6% of the Top 20 assets are above their 200-day moving average, a level we haven’t seen since the FTX collapse.

- 180-Day Lows: The number of assets hitting 180-day lows just recorded its second-worst reading since the Terra Luna collapse, with the worst in early August. Interestingly, fewer assets are making new lows now compared to last month, even though the market trades lower, signalling potential exhaustion.

All these breadth indicators combined suggest that the market appears to be searching for a floor, with signs of fatigue starting to emerge.

Seasonality

Though September has historically been a weak month, Bitcoin is about to enter its seasonally strong period in Q4. And while records can be broken, since 2016, Q4 in halving years has been particularly strong for Bitcoin.

The Improving Liquidity Outlook

This is where things get interesting. The liquidity landscape has turned decidedly supportive of crypto since August, even if the media’s fixation on rising U.S. recession fears suggests otherwise.

The first major signal? The U.S. Dollar has broken down through the critical support level at 101 on the DXY. While oversold in the short term, this move suggests that the liquidity spigots are about to open. A weaker dollar acts as a global economic release valve, easing the burden on economies saddled with U.S.-denominated debt — which is just about everyone at this point. Historically, a falling dollar sets the stage for Bitcoin to begin its next upward cycle — and this looks to be no exception.

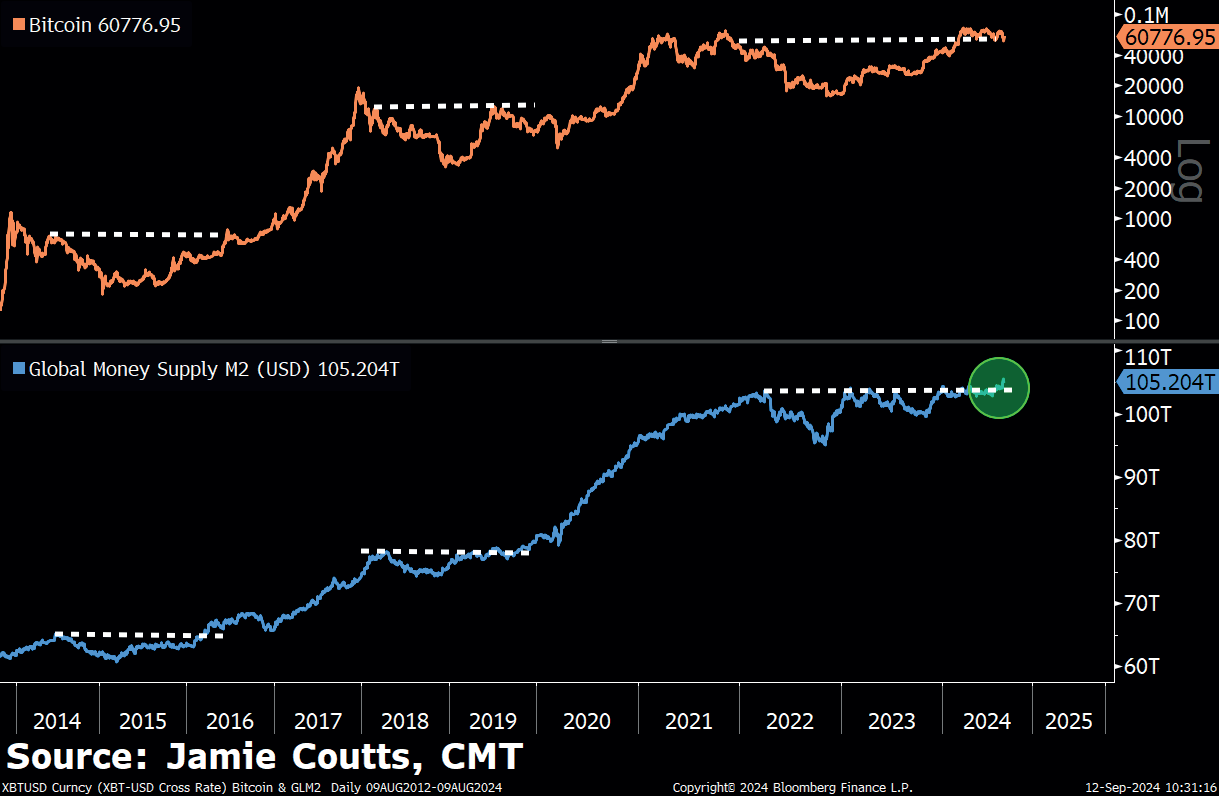

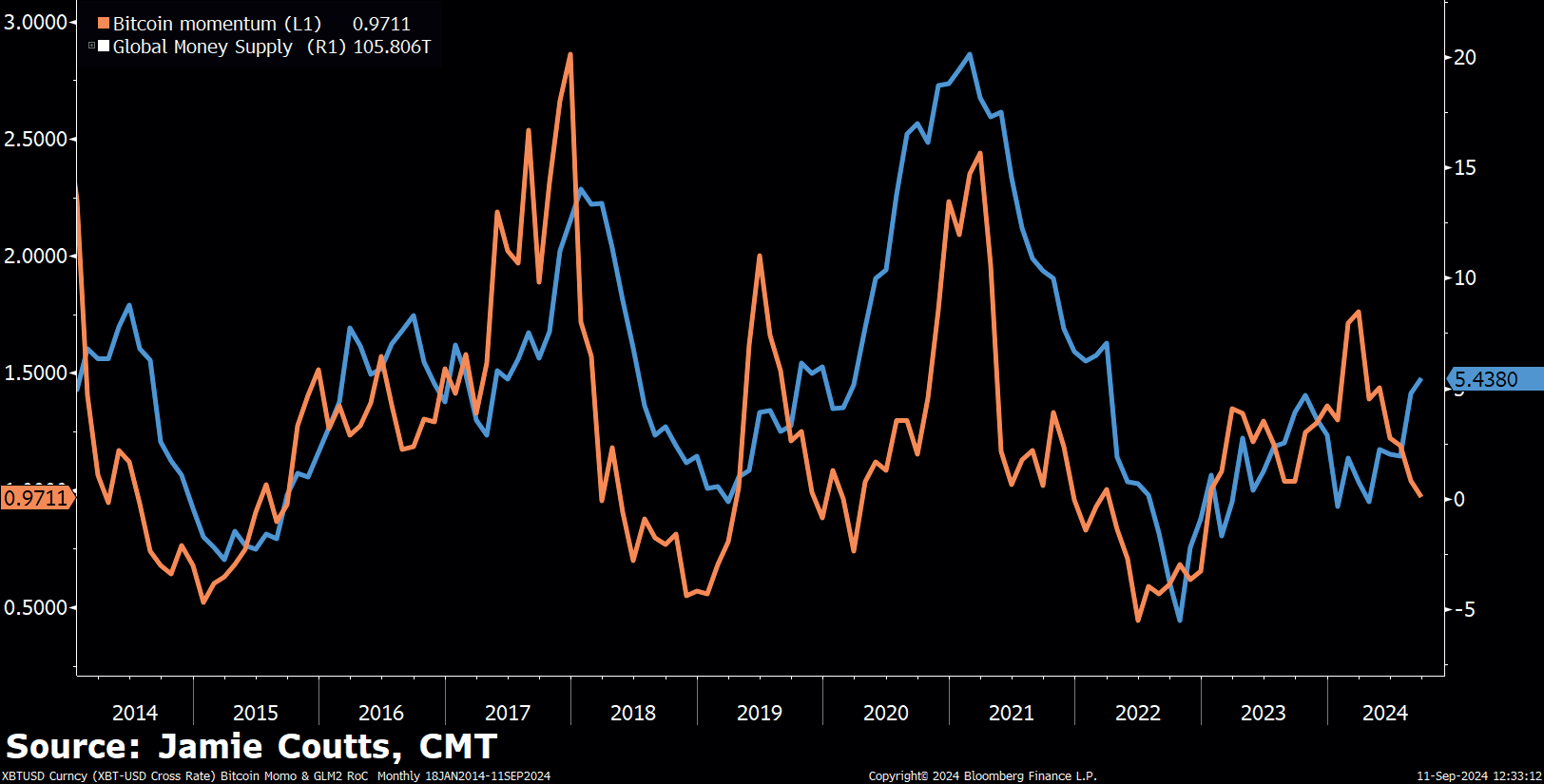

The weakening dollar is already making an impact on global money supply which has breached a 2.5-year resistance level. In a credit-based, fiat fractional reserve system, the money supply cannot contract for long — otherwise, the entire system risks collapse. Historically, when global M2 breaks resistance, it tends to increase for about two years, giving rise to the well-known 4-year cycle, or what Raoul and Julian call the “Everything Code.” Bitcoin, as usual, will be the first asset to sense when the music is about to stop, but that’s a problem for next year. Right now, it’s the opposite — the liquidity is moving higher after a long pause.

With yields collapsing (not shown) and the dollar weakening the rate of change on global M2 is now increasing once again. Bitcoin may be lagging for now, but this setup points to a high likelihood of a reversal in the coming quarter.

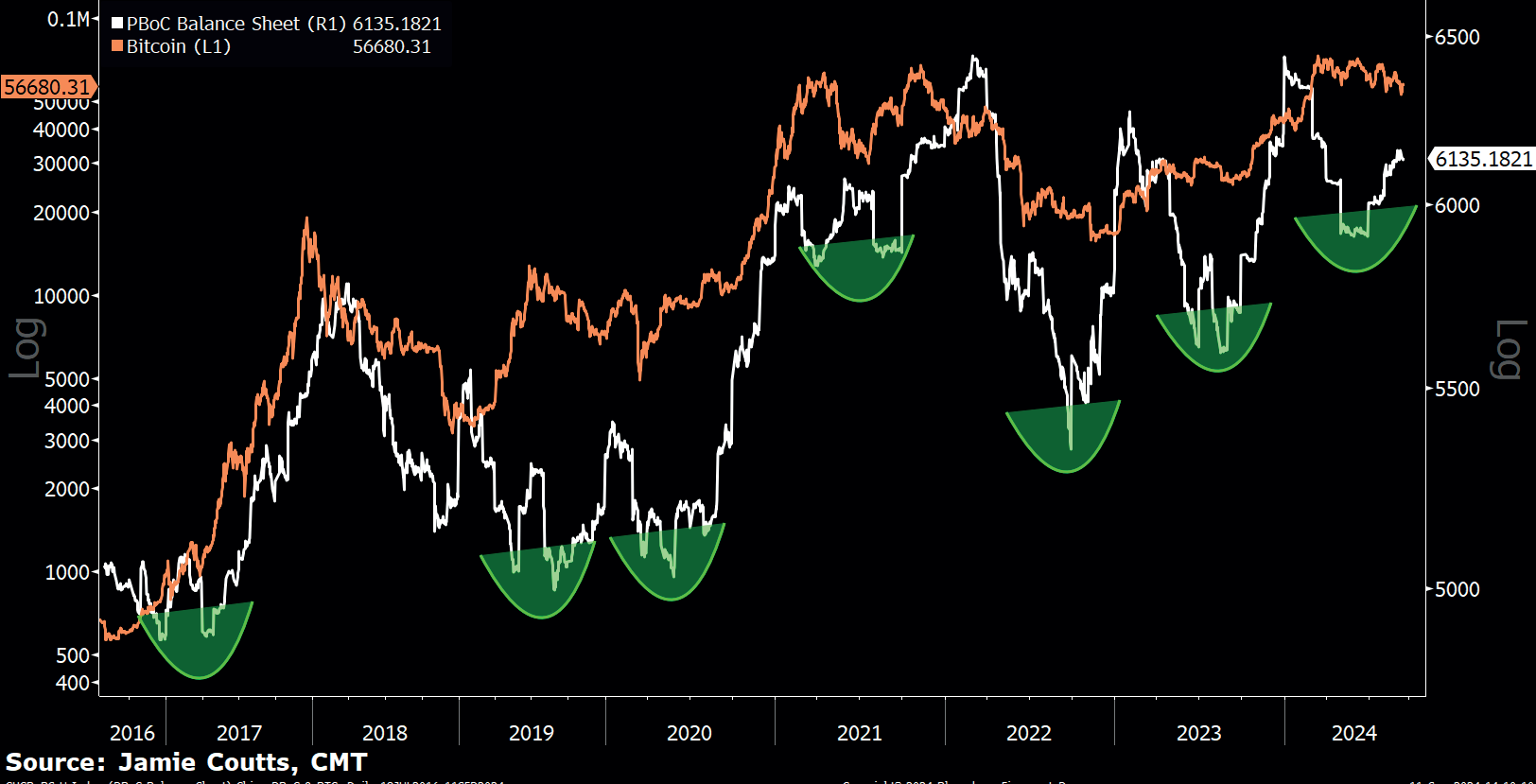

Behind the scenes, major central banks have been quietly coordinating liquidity injections. It started with China back in July, and now the Bank of Japan is following suit.

This brings us to my Macro State Indicator (MSI), which tracks synchronized periods of dollar weakness, global money growth, and central bank balance sheet expansion. In simpler terms, it’s a proxy for global liquidity. Last month, the MSI triggered its first bullish signal since November 2023, a signal that drove strong crypto gains until turning bearish in March of this year. Back-tested results from these signals have historically led to superior risk-adjusted returns compared to a long-only Bitcoin strategy.

The chart below shows the three MSI liquidity regimes (red = bearish, etc.), overlaid with ratio charts of Ethereum, SCP sector market cap, and Top 200 Equal weighted Index relative to Bitcoin. These are all different versions of the same theme — altcoin risk sentiment.

While historical data for these metrics is limited, a pattern emerges when liquidity is abundant, altcoins tend to outperform. It happened in 2020/21 during a sustained MSI bullish regime. And we saw a glimpse of this from November 2023 to March 2024, when altcoins ripped, and even ETH/BTC stopped falling.

Aligning with the modelling from Raoul and Julien suggests the bullish liquidity regime should extend well into 2025, which should, after a strong BTC move, see select Alts join in.

To read Jamie’s full report, sign up for Real Vision Pro Crypto using code BTC15 for your exclusive BTC Markets discount.

Get BTC Markets content delivered

Keep up to date with the latest from BTC Markets. Unsubscribe anytime.SubscribeFind out the latest crypto news