Welcome to your BTC Markets VIP Desk briefing.

The week in 60 seconds

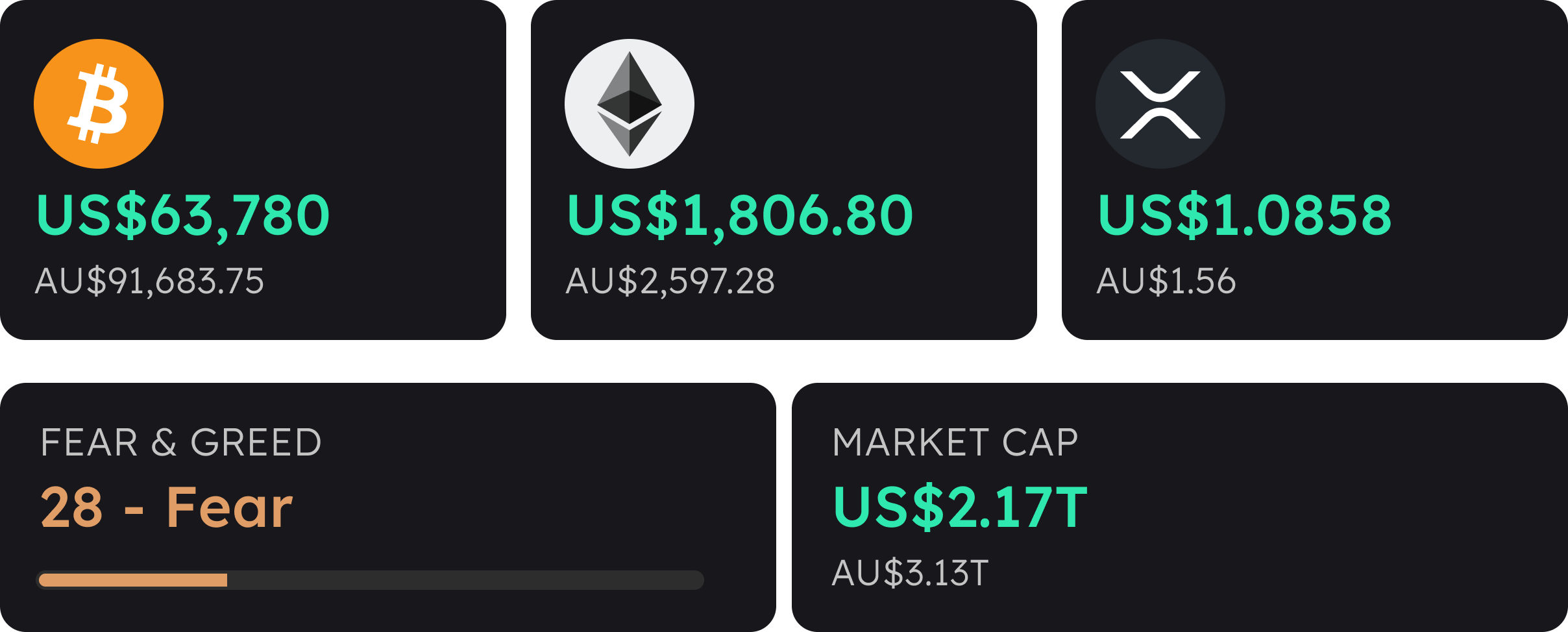

- Bitcoin reclaimed US$64,000 (~A$92,000) and Bitcoin ETFs posted their first weekly net inflow after a record-worst June of ~US$4 billion in outflows.

- Sentiment is recovering but still fearful. Fear & Greed sits at 26, up from 12 a month ago.

- Regulators moved on two fronts: the SEC proposed exemptions and a DeFi safe harbour; Ripple secured full MiCA authorisation in the EU.

- Macro dominates the week ahead: US CPI Tuesday night AEST, then Fed Chair Warsh's first testimony, with markets pricing a possible September hike.

- In Japan, a yen at four-decade lows is pushing listed companies to hold Bitcoin and XRP and even pay shareholder rewards in crypto.

Intro

Crypto held its ground in a hostile week. Bitcoin reclaimed US$64,000 even as oil jumped 5% and markets priced a possible Fed rate hike in September. ETF money quietly returned after the worst month on record. Now come the two biggest tests since June: Tuesday's US inflation print and Fed Chair Warsh's first testimony. Here's what matters and what to watch.

Market snapshot

Significant events

TLDR: Institutional flows turned, regulators offered clarity on two continents, and macro repriced towards tighter policy.

1. ETF flows flip positive after a record June exodus

The marginal institutional buyer has returned, tentatively.

June saw roughly US$4 billion leave US spot Bitcoin ETFs, the worst month since launch. July broke the pattern: US$265.7 million in on 6 July, US$90.4 million on 10 July, and the 7-day flow now positive. The 30-day picture is still deeply negative at - US$4.7B. This is a change in direction, not yet a change in regime. Inflows are concentrated in BlackRock's IBIT, suggesting institutions are re-engaging selectively. Whether they persist through this macro-heavy week is the clearest read on conviction.

2. Regulatory clarity advances on both sides of the Atlantic

The most accommodating US framework yet for token projects, plus major licensing wins for Ripple and Circle.

The SEC's proposal would let crypto startups operate under registration exemptions for up to four years, raise up to US$75 million a year without full registration, and use a DeFi safe harbour. Same week: Ripple completed full MiCA authorisation in the EU and Circle won OCC trust bank approval. The direction of travel is towards licensed, regulated crypto infrastructure on both continents. US and EU frameworks tend to set the template other jurisdictions, including Australia, adapt. The proposals still face comment periods, so timelines remain uncertain.

3. Markets reprice for a possible Fed hike as the Iran conflict reignites

The ceasefire ended, oil jumped 5%, and rate markets now price a meaningful chance of a September hike.

Renewed US-Iran strikes disrupted the Strait of Hormuz and sent WTI crude up around 5% for the week. With US inflation at 4.2% in May and June, FOMC minutes showing some officials favouring hikes, markets now price roughly a 60% chance of a quarter-point rise by September. Crypto has traded through this as a rate-sensitive asset first, an inflation hedge second. The sharpest recent drawdowns coincided with hawkish repricing, not the conflict itself. Equities have the AI trade to lean on; crypto has no earnings season, which is why Tuesday's CPI carries so much weight for digital assets.

By the Numbers

The Week in Data

270,000: BTC Accumulated by whale wallets over two weeks as bitcoin touched a 21-month low, the largest single accumulation spike ever recorded, larger than the COVID bottom and FTX collapse combined.

Source: Cpindesk / Bitfinex on-chain data

+US$170B: Added to total crypto market capitalisation in ten days as Bitcoin reclaimed US$64,000.

Source: Coingecko

1 billion: Weekly transactions on Solana for the first time, with active addresses near 7 million. Network usage sits at yearly highs while the token trades well below its peak.

Source: Solana network data via beIN crypto

¥162: Yen per US dollar, its weakest in roughly four decades and the force pushing Japanese corporate treasuries into Bitcoin and XRP.

Source: CoinDesk / FX markets

Market Sentiment

TLDR: Sentiment has climbed out of Extreme Fear for the first time in over a month. No longer panicking, not yet convinced.

Fear & Greed Index: 26 Fear, up from 23 (Extreme Fear) a week ago and 12 a month ago.

The recovery is the story, not the level. A reading of 26 is still firmly in Fear, but doubling from 12 in a month tracks the ETF flow reversal and the reclaim of US$64,000. The market is repricing from capitulation towards caution, which usually means choppy, headline-sensitive trading rather than clean trends.

The Signal

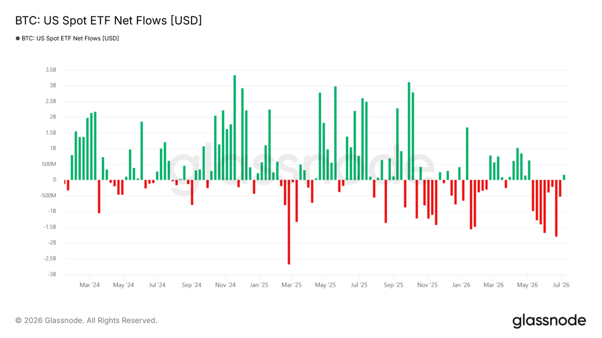

TLDR: Weekly Bitcoin ETF flows: June's record exodus giving way to July's tentative return. The cleanest visual of the institutional turn.

Source: CoinGlass Bitcoin ETF Fund Flows | Spot BTC Net Inflow & Holdings |

US Spot Bitcoin ETF: Weekly Net Flows

A wall of red outflow bars through June, roughly US$4 billion and the worst month on record, flips to green inflow to start July. Sustained green through Tuesday's CPI and the Warsh testimony would show institutional demand surviving a macro stress test; a return to red would suggest July's recovery was tactical, not conviction.

Economic calendar

TLDR: Tuesday night AEST delivers the month's two biggest events back-to-back: US CPI, then Fed Chair Warsh's first testimony.

14 July: US CPI (June)

Consensus: headline eases to ~3.9%, core near 2.9%. Both remain well above target. A hot print strengthens the hike case and pressures crypto; a soft print does the opposite.

15 July: Fed Chair Warsh: House testimony

Warsh's first testimony since taking the chair, 90 minutes after CPI. He has ruled out forward guidance, so markets will parse tone. Senate follows Thu ~12:00am AEST.

15 July: US PPI, Fed Beige Book & China Q2 GDP

PPI flags pipeline inflation; China's GDP shapes commodity demand and the AUD. Bank of Canada also decides rates.

16 July: US Retail Sales & Jobless Claims

The consumer health check. Resilient spending gives the Fed room to tighten; softness supports a hold.

18 July: Michigan Consumer Sentiment (prelim)

First read on how households are absorbing the energy shock. Its inflation expectations feed the Fed debate.

All week: US Q2 bank earnings & US-Iran developments

Major banks report Tuesday-Thursday. Any move around the Strait of Hormuz flows through oil into the rates picture. No RBA meeting this week; markets price modest tightening for August.

From the Desk

TLDR: Crypto is caught between a genuine internal recovery and a macro test it doesn't control. Tuesday tells us which force is stronger.

Two stories are running in opposite directions. Inside crypto, the internals have improved: ETF flows positive, sentiment doubled off its June low, and demand emerging from new places: Japanese corporate treasuries, Solana's record network usage, regulatory progress in the US and EU. This is what early repair looks like: unglamorous, selective, easily interrupted.

Outside crypto, the macro has hardened. Inflation above 4%, a Fed debating hikes rather than cuts, and oil hostage to the Strait of Hormuz make the least crypto-friendly rate backdrop since 2022. Crypto has no earnings season to hide behind. That's why Tuesday matters more to digital assets than to almost any other market. A soft CPI print removes the single largest weight on the asset class; a hot one tests whether July's buyers have conviction or were covering shorts. ETF flows in the days after the print will be the most honest answer. We suspect the market's character for the rest of Q3, repair or relapse, gets decided this week.

Question of the week

“Bitcoin ETFs just had their worst month on record. So why did the Bitcoin price go up in July?”

ETF flows measure one group of buyers, US institutions, not the whole market. June's US$4 billion in outflows was absorbed by others: traders covering shorts, offshore buyers, and corporate treasuries like Japan's Metaplanet, which kept accumulating through the weakness. When ETF selling slowed and reversed in early July, the pressure lifted, and a short squeeze did the rest. ETF flows are one input into price, not a mechanical driver. The two rhyme over months but can diverge over weeks.

Have a question? Reply to this email and we may feature it in a future edition.

Story of the week

Dividends, but Make Them Bitcoin

TLDR: With the yen at a four-decade low, Japanese companies are holding Bitcoin and XRP. Some are paying shareholder rewards in it.

The yen is trading near 162 to the US dollar, its weakest in roughly forty years, and corporate Japan is responding by buying crypto. SBI VC Trade, the crypto arm of Tokyo giant SBI Holdings, just passed 2 million accounts, double a year ago, with much of the growth from companies moving cash reserves into Bitcoin and XRP. Tokyo-listed Metaplanet now holds ~43,000 BTC, the third-largest public holding in the world.

The most Japanese twist is what some firms do with the coins. Listed companies are distributing Bitcoin or XRP through kabunushi yūtai, the country's beloved shareholder-perk programs that traditionally hand out rice vouchers and theme-park tickets.

Somewhere in Japan, an investor who once received a gift hamper for holding shares is now receiving Bitcoin instead. That is crypto entering the most conservative corner of a conservative financial culture, not as speculation but as a practical answer to a weakening currency.

Thank you for reading. Reach out anytime if you would like to discuss this week's content.

Disclaimer: The information provided on this page is issued by BTC Markets Pty Ltd (BTC Markets, we, us, our). The information is general only and is not intended to constitute an opinion or recommendation with respect to its contents. Past performance is not a reliable indicator of future performance. Any reference to past performance is intended to be for general illustrative purposes only. The information cannot be relied upon for any purposes and is not intended to be a substitute for professional advice.

The information does not purport to be complete, accurate or contain all of the information that a person may require to make a decision. It may also contain forward looking statements, which are subject to known and unknown risks, uncertainties, and other factors. We recommend you obtain professional advice before making any decision with respect to the matters discussed in this document. To the maximum extent permitted by law, BTC Markets will have no liability for any loss or liability of any kind: (i) arising in respect of the information contained (or not contained) on this page; or (ii) arising from a person relying on any information or statement contained on this page. The information provided is only intended for recipients in Australia. This information cannot be reproduced without our prior written permission.

Get BTC Markets content delivered

Keep up to date with the latest from BTC Markets. Unsubscribe anytime.SubscribeFind out the latest crypto news

Trading fees promotion T&Cs (8 July 2026)