Weekly crypto wrap: 31st October 2024

TLDR

- Bitcoin reaches a high of AU$110,500, levels not seen since March 2024.

- Real Vision Navigating the bull: Liquidity-driven crypto cycle projections.

- US spot BTC ETF sees record single-day net inflow of US$870m.

- New mobile app release: in-app card deposits!

- Unlock personalised, secure, and efficient OTC crypto transactions.

- BTC Markets’ CEO to speak at the Singapore FinTech Festival 2024.

- Sui emerges as a notable contender, gaining traction among decentralised finance platforms.

BTC Markets announcements

ICYMI: New mobile app release – in-app card deposits!

Last week, we launched a convenient new feature on the BTC Markets mobile app: in-app card deposits. Now you can easily and securely deposit AUD to your account using an Australian-issued VISA or Mastercard credit or debit card.

Here’s what’s new:

- Simple and secure deposits powered by Stripe

- Apple Pay card deposits available for iOS users

- Link deposits available on both iOS and Android

- Input validation to minimise errors

Fully verified customers can update to the latest app version or download the app from the App Store (iOS) and Google Play (Android) to start using card deposits.

For a step-by-step guide, see our help article on ‘How to deposit using a bank card’.

Read the announcement here.

Real Vision Deep Dives with Chief Crypto Analyst, Jamie Coutts.

Navigating the bull: Liquidity-driven crypto cycle projections.

We're excited to share the latest Deep Dive preview from Real Vision’s Chief Crypto Analyst, Jamie Coutts. In this report, he discusses the impact of central banks’ extensive liquidity injections. A topic of growing significance as global financial systems navigate inflation, economic slowdowns, and currency instability.

Well, folks, the time has come. After a six-month hiatus, central banks are once again flooding the markets with liquidity as leverage and expectations reset, setting the stage for the next wave of the crypto bull market.

Before fear and greed take over, I’ve decided to map out what might lie ahead over the next 12 months or so. We’ll start by examining the liquidity cycle, then forecast Bitcoin, and finally explore broader sectors. This report is extensive, so while detailed analysis of the pockets of the market I expect to outperform will be covered in the next report, I will provide projections for sectors I believe will excel and price targets for my top assets—ETH, BTC, SOL, SUI, and NEAR—where my conviction is strongest. As I refine my modelling, future reports may adjust these targets.

Read the preview of Jamie’s report: Navigating the bull: Liquidity-driven crypto cycle projections | BTC Markets

BTC Markets shortlisted for DECA Blockies Award!

We’re excited to share that BTC Markets has been named a finalist for the Digital Currency Exchange of the Year at the prestigious Digital Economy Council of Australia (DECA) Blockies Awards!

This nomination reflects our dedication to providing a secure, reliable, and innovative trading platform for our clients, and we’re honoured to be recognised alongside the industry’s best.

The awards ceremony will take place in Sydney on November 21st, followed by an afterparty to celebrate with leaders from across the blockchain community. Thank you for being a part of BTC Markets’ journey – we couldn’t have achieved this without your support!

If you'd like to join us, tickets are available here.

2024 Singapore FinTech Festival: Financial crime: Anatomy of a scam.

BTC Markets CEO, Caroline Bowler will be a key panellist at the Singapore FinTech Festival, the world’s largest FinTech event. Appearing alongside Rene Michau, Global Head of Digital Assets at Standard Chartered, Amanda Wick, Principal at Incite Consulting, and Dina Mainville, Founder and President of Collisionless.

In this session, they will discuss "Financial Crime: Anatomy of a Scam" on Friday, 8 November, at the Regulation Stage. Don’t miss this chance to gain valuable insights into the pressing challenges facing the industry!

Experience seamless trading: Unlock personalised, secure, and efficient OTC crypto transactions with us.

When it comes to large-scale crypto transactions, trading over the counter (OTC) with us offers a streamlined, secure, and personalised experience that other exchanges simply can't match. Our OTC desk minimises slippage and ensures deep liquidity, so you can execute sizable trades without the worry.

With our expert traders by your side, we tailor each trade to meet your specific goals. We prioritise speed and compliance, meaning you can lock in optimal prices with the comfort of full regulatory assurance.

Book a call with your OTC expert today.

BTC Markets in the news

AFR: Donald Trump bets see investors pile into bitcoin, gold to record levels.

Spot Bitcoin exchange-traded funds in the US have attracted about $US3.6 billion in net inflows this month. In options markets, traders are ramping up bets that Bitcoin will hit $US80,000 by the end of November.

“The rally has been largely fuelled by inflows into US bitcoin ETFs… making Bitcoin more accessible for traditional investors and driving price pressure through supply reduction,” said Rachael Lucas, an analyst at Australia’s largest crypto exchange, BTC Markets.

However, BTC said its trading volumes were still below peak levels in 2021, suggesting retail investors remain cautious."

State of crypto

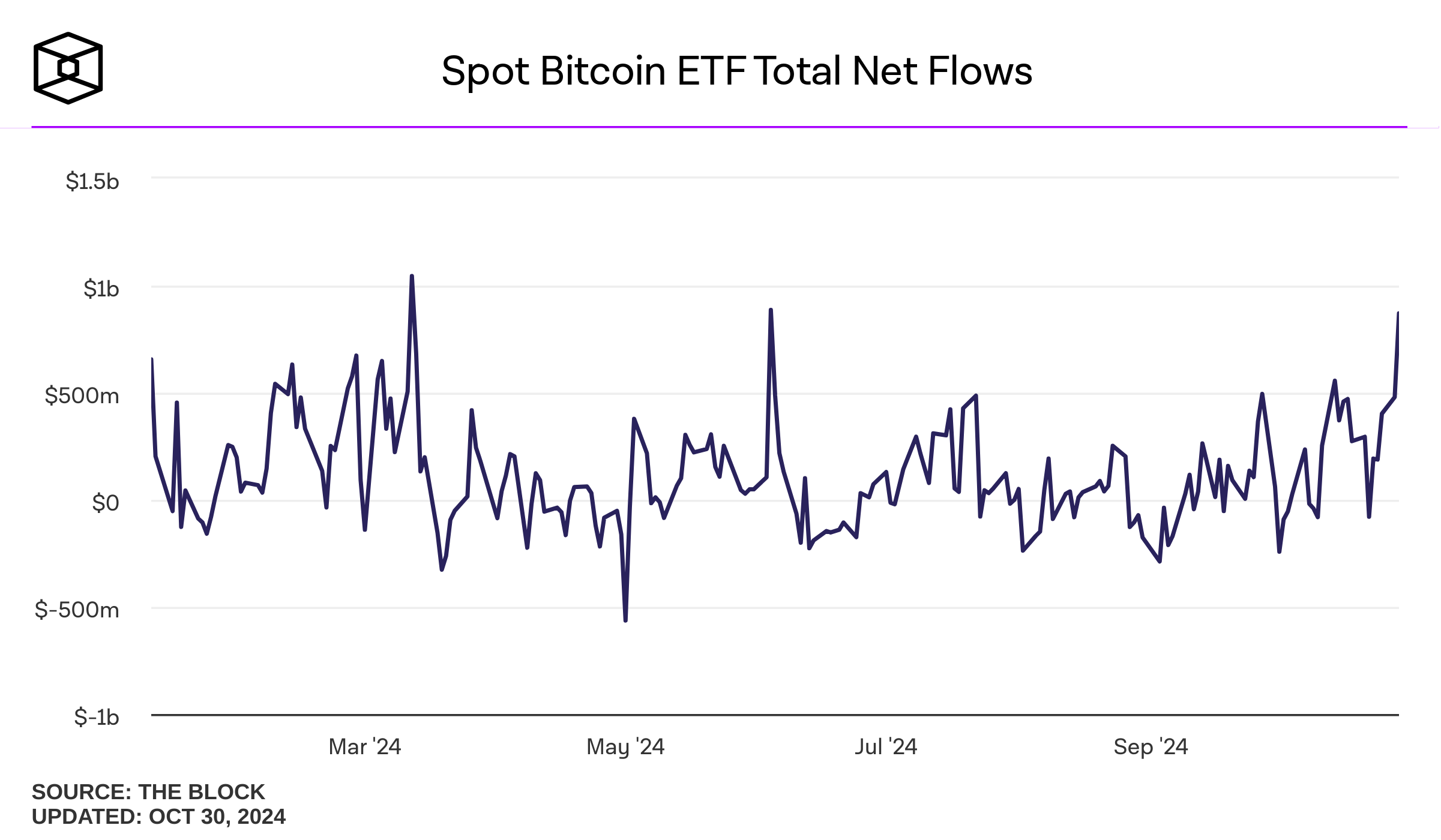

- US spot BTC ETF sees record single-day net inflow of US$870m.

- Institutional players are leading the charge in Bitcoin ETF growth and adoption.

- Strong momentum suggests a bright future for Bitcoin and cryptocurrency market expansion.

- Sui emerges as a notable contender, gaining traction among decentralised finance platforms.

The weekly trading stats as of Monday, October 28th at 11:00 am AEDT, based on data from Tradingview in USD.

US spot BTC ETF sees record single-day net inflow of US$870m.

The latest data from Eric Balchunas, Senior ETF Analyst for Bloomberg reveals that BlackRock's ETF, identified by its ticker symbol $IBIT, has surpassed the US$30 billion mark in AUM following substantial inflows and price appreciation of Bitcoin. Notably, $IBIT achieved this impressive feat in just 293 days, making it the fastest-growing ETF in history, outpacing the previous record, which took 1,272 days to achieve. To put this achievement into perspective, even the popular gold ETF, GLD, took 1,790 days to reach a similar milestone.

Buy BTC/AUD on BTC Markets.

Institutional players lead the charge.

The current momentum can be attributed to the growing involvement of institutional players such as BlackRock, VanEck, and Fidelity Investments in the digital asset landscape. Their participation is making Bitcoin more accessible to traditional investors, subsequently driving price appreciation through supply reduction.

According to Matthew Sigel, Head of Digital Assets Research at VanEck, this bullish environment is particularly timely as the upcoming presidential election approaches. Sigel emphasises that former President Donald Trump appears to be the more pro-crypto candidate, especially considering the prevailing conditions of money growth and market seller exhaustion. Additionally, the recent expansion of BRICS membership may enable these countries to leverage government resources for Bitcoin mining, potentially positioning Bitcoin as a pivotal asset for settling global trade.

Source: TheBlock.co

A bright future for Bitcoin?

Looking ahead, Sigel suggests that the aftermath of the election could act as a significant catalyst for Bitcoin's growth. By the year 2050, he envisions Bitcoin evolving into a widely accepted reserve asset, utilised in global trade and by central banks, with an ambitious price target of US$3 million per Bitcoin.

As of October 29, U.S. spot Bitcoin ETFs reported an impressive US$867 million in net inflows, marking the largest single-day inflow since June 5. The trading volume for these ETFs has soared past US$4.5 billion, with BlackRock leading the pack at over US$3.3 billion. Recent Bitcoin price action has also been bullish, as the cryptocurrency has rallied 2.63% to exceed the US$70,000 threshold for the first time since June.

Source: @WatcherGuru

ETF growth momentum continues.

These inflows are pivotal for alleviating oversupply risks and could drive Bitcoin to new heights as demand surges. Current estimates suggest that U.S. spot ETFs may accumulate 1 million Bitcoin by next week, which, at a price of US$77,000 per Bitcoin, would equate to US$72 billion. This would surpass the holdings of Satoshi Nakamoto, Bitcoin's mysterious creator, by mid-December, marking a significant milestone ahead of the ETFs' first anniversary.

Source: @EricBalchunas

While these ETFs are currently adding around 17,000 BTC weekly, market volatility could influence this trajectory. A sudden sell-off could hinder progress, but if Bitcoin prices maintain their upward momentum and political developments, such as a potential Trump victory, unfold favourably, fear of missing out (FOMO) could accelerate accumulation.

Bitcoin’s rise in 2024: a strong year with election insights.

According to The Kobeissi Letter, a popular market analyst, Bitcoin has surged over 60% this year, positioning it among the top-performing assets of 2024. Over the past 12 months, the cryptocurrency market has added $1.5 trillion to its market cap, and Bitcoin alone has outperformed the S&P 500 by 2.5 times.

Contrary to initial concerns about the impact of the U.S. election, Bitcoin has gained traction, benefiting from growing political support. Historical data shows that Bitcoin prices rose significantly post-elections, with gains of 10,000% after 2012 and 2,600% after 2016.

Source: @kobeissiletter

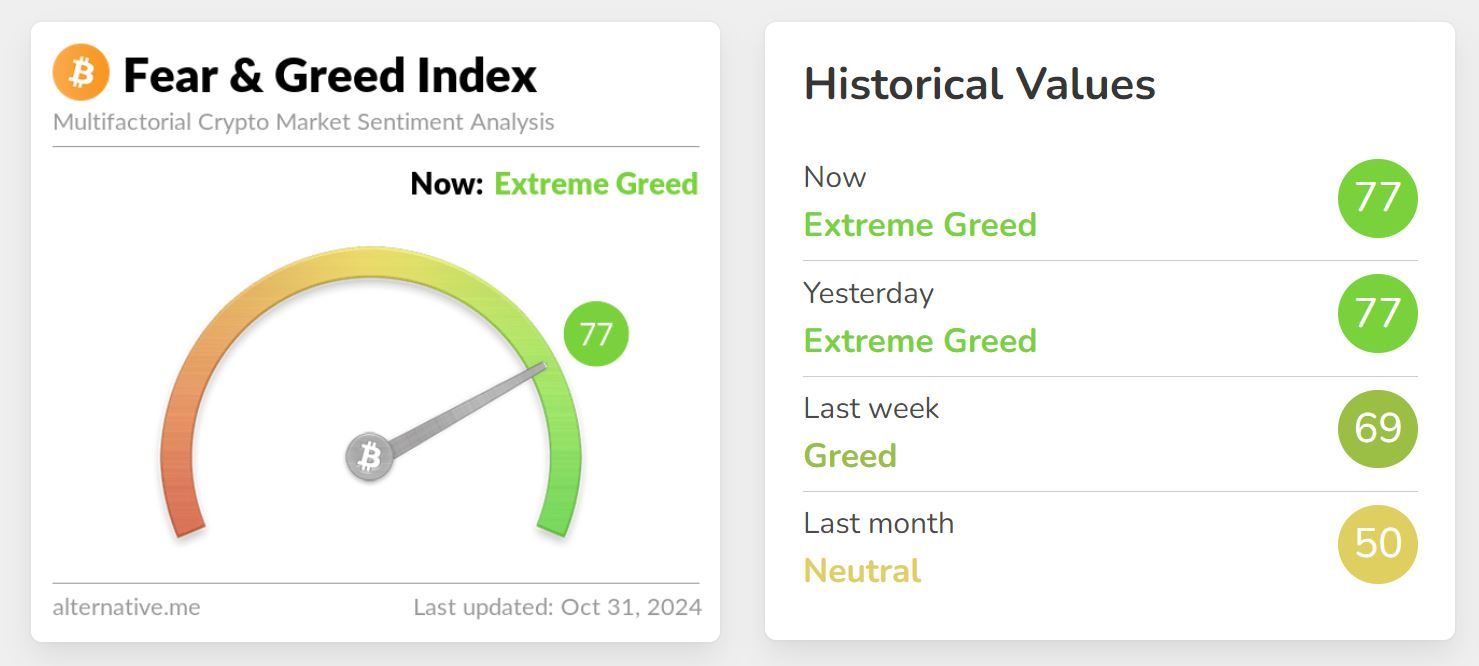

This rally is primarily fuelled by institutional interest, as seen in high open interest levels (now at $22.7 billion) and minimal retail involvement thus far. The current sentiment index reads at 77 (Extreme Greed), which may caution traders as historically high greed levels have sometimes preceded market corrections. With the election approaching, heightened volatility in crypto markets is anticipated.

Emerging contenders: Sui rises.

Sui has recently gained attention, surging 13% on October 29t. This uptick coincided with Bitcoin surpassing the US$71,000 mark, resulting in over US$3 million in short liquidations and increased open interest in futures contracts.

Sui's decentralised exchanges processed US$4.47 billion in tokens this month, marking its entry into the top ten blockchains. With a total value locked of US$944 million, Sui is making waves in both the DeFi and gaming sectors, bolstered by strategic initiatives and the launch of Sui Bridge.

Trade SUI/AUD on BTC Markets.

Crypto Fear & Greed Index

Source: Fear & Greed Index

The week ahead: economic events

Thursday, October 31st

- 11:30am China NBS Manufacturing PMI

- 1pm Japan Interest Rate

- 5:45pm France Inflation Rate

- 8pm Euro Area Inflation Rate

- 8pm Italy Inflation Rate

- 10:30pm United States Core PCE Price Index MoM, Personal Income & Personal Spending

Friday, November 1st

- 10:30am Australia Building Permits MoM, Home Loans, Investment Lending for Homes, Producer Price Inflation QoQ & YoY, Private House Approvals MoM

- 11:45am China Caixin Manufacturing PMI

- 10:30pm United States Non-Farm Payrolls & Unemployment Rate

- 3:30pm Australia Commodity Prices YoY

Saturday, November 2nd

- 12am United States ISM Manufacturing PMI

Monday, November 4th

- 8am Australia Judo Bank Services & Bank Composite PMI

- 10:30am Australia ANZ-Indeed Job Ads MoM

Tuesday, November 5th

- 1:30pm Australia Interest Rate

- 11:30pm Canada Balance of Trade

Wednesday, November 6th

- 1am United States ISM Services PMI

- 8am Australia Ai Group Industry, Construction & Manufacturing Index

- 11am Australia Melbourne Institute Inflation Gauge MoM

Source: trading economics

Market reflections

Overview

Australia's inflation has cooled to a three-year low, with Q3 CPI growth slowing to just 0.2%. In the US, BlackRock's CEO discusses mixed economic trends amid declining job openings and cautious durable goods orders. Germany's inflation rises to 2%, raising recession concerns, while Japan's consumer confidence dips to its lowest level since May. The Eurozone achieves its strongest quarterly growth in two years, driven by robust performance in Spain and Ireland, while France's economy grows by 0.4% in Q3 2024, supported by solid consumer spending despite ongoing economic uncertainties.

Australia

- Australia’s inflation cools off to a three-year low

- CPI growth slows to just 0.2% in Q3

Australia’s inflation cools to a three-year low as CPI growth slows to just 0.2% in Q3.

Australia’s inflation rate just took a significant step back, with the Consumer Price Index (CPI) rising only 0.2% in the September quarter, its lowest bump since mid-2020. Annual inflation has dropped to 2.8%, down from 3.8% last quarter, putting us well within the Reserve Bank of Australia’s 2-3% target range. This big dip is thanks in large part to steep falls in electricity prices (-17.3%) due to government rebates and a 6.7% drop in fuel costs.

While underlying inflation eased to 3.5%, services inflation still sits at a higher 4.6%, showing that some sectors are still feeling price pressure. Overall, though, these results indicate a promising turn in inflation—hopefully making life a little easier for Australians.

Global

- BlackRock's CEO discusses US inflation, interest rates, and mixed economic trends.

- Job openings decline and durable goods orders signal caution in consumer sectors.

- Germany's inflation hits 2% as GDP rebounds, raising recession concerns ahead.

- Consumer confidence improves slightly, but economic uncertainty keeps outlook fragile.

- Japan's consumer confidence dips to lowest level since May.

- Eurozone sees strongest quarterly growth in two years, driven by Spain and Ireland.

- French economy grows 0.4% in Q3 2024, boosted by robust consumer spending.

United States

Larry Fink’s insights on inflation and interest rates.

Larry Fink, CEO of BlackRock, stated at Saudi Arabia’s Future Investment Initiative that he anticipates the U.S. Federal Reserve will likely implement only one additional interest rate cut in 2024. Fink highlighted “embedded inflation” as a primary factor constraining rate reductions, driven by policy changes like onshoring and government investments that keep price pressures elevated.

US Q3 growth dips to 2.8% amid mixed spending and investment trends.

The US economy grew by an annualised 2.8% in Q3 2024, falling just short of expectations and the previous quarter’s 3% growth, according to the Bureau of Economic Analysis.

Consumer spending surged, especially on goods like motor vehicles and prescription drugs, marking the fastest growth since early 2023. Government spending also increased, driven largely by defence, while exports and imports saw notable gains.

However, the economy was weighed down by a slowdown in private inventories and fixed investment, particularly in construction and residential areas, despite a robust increase in equipment investment. Overall, the economy showed resilience but with some areas of mixed performance.

Job openings hit lowest since 2021, cooling labour market signals caution for consumer-driven sectors.

In September, U.S. job openings dropped significantly, falling by 418,000 to 7.443 million, the lowest since January 2021, highlighting a cooling labour market.

This decline was sharper than expected, as the market had anticipated about 7.99 million openings. Key sectors experiencing decreases included health care and social assistance (-178,000), state and local government excluding education (-79,000), and federal government (-28,000). In contrast, job openings in finance and insurance rose by 85,000, suggesting growth in that sector.

The cooling job market can signal a slowdown in consumer spending, potentially impacting earnings in consumer-driven sectors and affecting broader economic stability.

US durable goods orders signal mixed economic health amid transportation sector struggles.

The 0.8% drop in durable goods orders in September, particularly driven by a significant decrease in transportation equipment, could indicate broader economic weakness. This decline may prompt caution among retail investors assessing industrial sectors.

While the transportation sector struggled, the rise in orders for non-defence capital goods (excluding aircraft) by 0.5% suggests that business spending plans are more robust than expected. This could signal potential growth in the broader economy. The increase of 0.4% in new orders excluding transportation highlights resilience in other areas.

Germany

Germany’s inflation rises to 2% as GDP rebounds slightly, but recession fears loom.

In October, Germany's annual inflation rate accelerated to 2%, the highest level in three months, up from a 3.5-year low of 1.6% in September and surpassing expectations of 1.8%. This increase was driven by a faster rise in prices for services (up 4%) and food (up 2.3%), alongside a modest rebound in goods prices. Energy costs continued to decline, but at a slower pace (-5.5% vs. -7.6%). On a monthly basis, the Consumer Price Index rose by 0.4%, contrasting with a flat reading in September.

In terms of economic performance, Germany's GDP grew by 0.2% in Q3, rebounding from a sharper 0.3% contraction in the previous quarter and outperforming forecasts of a 0.1% decline.

However, on a year-on-year basis, the economy shrank by 0.2%, marking the sixth consecutive quarter without growth. The German government projects a further 0.2% contraction for 2024, indicating the potential for the country to experience its first two-year recession since the early 2000s.

Challenges such as high energy prices, weak external demand, and competitiveness issues in the auto sector are contributing to this outlook. Despite these headwinds, a projected recovery in 2025 is anticipated, driven by improved private consumption and renewed demand for industrial exports.

German consumer confidence rises but remains fragile amid economic uncertainty.

German consumer confidence is recovering, with improvements in income expectations and a greater willingness to buy, both reaching their highest in nearly three years. However, persistent concerns, like inflation and geopolitical crises, alongside rising company insolvencies and job cut plans, may dampen this momentum.

Germany’s business climate brightens slightly but economic challenges remain.

October’s uptick in Germany’s Ifo Business Climate Index could bolster investor confidence, suggesting a short-term stabilisation in Europe’s largest economy. This may influence stock markets positively in the near term.

Service sectors, including logistics, tourism, and IT, showed improved sentiment, which might indicate growth opportunities in these areas. The manufacturing sector’s challenges persist with low-capacity utilisation and weak orders.

Germany’s manufacturing sector shows signs of recovery, but caution remains for investors.

The HCOB Flash Germany Manufacturing PMI rose to 42.6 in October from 40.6 in September, indicating a minor rebound but still reflecting a deep contraction. Reports of reduced consumer spending due to economic uncertainty, particularly in the auto sector, suggest ongoing challenges. Significant drops in factory gate charges and purchase prices indicate competitive pressures in the market.

Japan

Japan's consumer confidence dips to lowest level since May.

Japan's consumer confidence index took a step back in October, dropping to 36.2 from September's five-month high of 36.9, falling short of market expectations of 37. This marks the lowest level of consumer morale we've seen since May.

The decline is driven by a drop in household sentiment across all areas: income growth slipped to 39.4 from 40.1, employment edged up slightly to 41.6 from 41.4, willingness to buy durable goods fell to 29.7 from 31.0, and overall livelihood dropped to 34.2 from 34.4.

Euro Area

Eurozone achieves strongest quarterly growth in two years, led by Spain and Ireland.

The Eurozone’s economy expanded by 0.4% in Q3 2024, marking its fastest quarterly growth rate in two years and exceeding forecasts of 0.2%. Key contributors included Germany, which narrowly avoided recession with 0.2% growth, and robust performances from France (up 0.4%) and Spain (steady at 0.8%). Ireland posted a notable recovery, expanding by 2% after a 1% contraction in Q2.

Despite these gains, Italy’s GDP stalled, and Latvia remained in contraction. On an annual basis, the Eurozone economy grew by 0.9%, the strongest pace since early 2023 and above expectations, showing resilience in the face of economic headwinds. The European Central Bank’s 0.8% growth target for 2024 now appears within reach.

France

French economy surges with 0.4% growth in Q3 2024, powered by consumer spending.

The French economy expanded by 0.4% in Q3 2024, accelerating from 0.2% in Q1 and exceeding the 0.3% forecast. This growth was driven primarily by strong domestic demand, with household consumption rising 0.5% due to the Paris Olympics. Government spending also increased by 0.5%.

However, both exports and imports declined, while fixed investment dropped 0.8%. Year-on-year, the economy grew 1.3%, outperforming the previous quarter's 1.1% growth. Overall, France’s GDP growth has averaged 3.04% from 1950 to 2024, with a peak of 17.4% in Q2 2021.

Italy

Italy’s economy grinds to a halt in Q3, raising questions for 2024 growth targets.

Italy's economy showed no growth in the third quarter of 2024, a slowdown from the modest 0.2% growth seen in Q2 and falling short of market expectations for another 0.2% gain. The stagnation marks the first flat quarter since a contraction in mid-2023, highlighting the impact of the European Central Bank’s restrictive borrowing costs.

While inventory growth added positively to the economy, this was offset by weaker net foreign demand, stalling overall GDP progress. Annual growth reached just 0.4% in Q3, the slowest pace since late 2020, casting doubt on the government's target of 1% growth and its 3.8% deficit goal for 2024.

Scam awareness

AI-powered crypto scams: the next generation of fraud.

As technology evolves, so do the tactics of scammers. In a recent article, blockchain analytics firm Elliptic reported a concerning trend: the rise of AI-powered crypto scams.

These scams leverage artificial intelligence to create convincing deepfakes, scam tokens, phishing websites, and spread disinformation. While the current risk is relatively small, it is crucial for crypto users to be vigilant and take necessary precautions to protect themselves.

Read our blog article here.

The ASIC provides a checklist of common scams and ways to avoid them. To learn more, visit ASIC’s website.

Discover more on our ‘Compliance conversation’ blog page, where we share the latest updates on safeguarding against scams and protecting your assets. Stay informed and stay protected!

Want to get on our mailing list?

Sign up for free and join over 362,000 Australian traders who receive the BTC Markets Weekly Crypto Wrap.

Feedback

If you have any feedback on our newsletter or want to request specific content, please submit a support ticket and we will respond shortly.

Disclaimer: The information provided on this page is issued by BTC Markets Pty Ltd (BTC Markets, we, us, our). The information is general only and is not intended to constitute an opinion or recommendation with respect to its contents. Past performance is not a reliable indicator of future performance. Any reference to past performance is intended to be for general illustrative purposes only. The information cannot be relied upon for any purposes and is not intended to be a substitute for professional advice.

The information does not purport to be complete, accurate or contain all of the information that a person may require to make a decision. It may also contain forward looking statements, which are subject to known and unknown risks, uncertainties, and other factors. We recommend you obtain professional advice before making any decision with respect to the matters discussed in this document.To the maximum extent permitted by law, BTC Markets will have no liability for any loss or liability of any kind: (i) arising in respect of the information contained (or not contained) on this page; or (ii) arising from a person relying on any information or statement contained on this page. The information provided is only intended for recipients in Australia. This information cannot be reproduced without our prior written permission.

Get BTC Markets content delivered

Keep up to date with the latest from BTC Markets. Unsubscribe anytime.SubscribeFind out the latest crypto news