Deep Dives with Real Vision’s Chief Crypto Analyst, Jamie Coutts

October 18, 2024

To read Jamie’s full report, sign up for Real Vision Pro Crypto using code BTC15 for your exclusive BTC Markets discount.

Navigating The Bull: Liquidity-Driven Crypto Cycle Projections

Introduction

Well, folks, the time has come. After a six-month hiatus, central banks are once again flooding the markets with liquidity as leverage and expectations reset, setting the stage for the next wave of the crypto bull market.

Before fear and greed take over, I’ve decided to map out what might lie ahead over the next 12 months or so. We’ll start by examining the liquidity cycle, then forecast Bitcoin, and finally explore broader sectors. This report is extensive, so while detailed analysis of the pockets of the market I expect to outperform will be covered in the next report, I will provide projections for sectors I believe will excel and price targets for my top assets—ETH, BTC, SOL, SUI, and NEAR—where my conviction is strongest. As I refine my modelling, future reports may adjust these targets.

One thing is certain: I will be wrong. Forecasting markets with precision is a fool’s errand, and the exact numbers and dates are bound to miss the mark. However, this exercise has been invaluable in prompting me to think through various scenarios and assign probabilities. While my inputs could be wildly off, adopting a probabilistic approach helps keep emotions in check as markets do their thing. The goal isn’t perfection; it’s to be directionally correct within a reasonable margin of error.

Secular Themes

My entire framework for digital assets rests on two powerful, long-term trends: currency debasement and unrelenting technological adoption. These secular forces are reshaping the global economy and creating fertile ground for digital assets to thrive.

Currency debasement is a constant in a fiat system, but as debt levels rise, central banks are forced to accelerate liquidity injections. Depending on the form factor, this drives asset and eventually goods inflation, eroding the value of fiat currencies. As purchasing power declines, more investors are forced to seek alternatives—particularly hard assets like Bitcoin, which is increasingly viewed as digital gold in an era of rampant money printing.

On the flip side, technological adoption continues its exponential march forward. From blockchain to AI, disruptive technologies are integrating deeper into the fabric of industries, creating new efficiencies and redefining what’s possible. Crypto, and blockchain networks, particularly, are at the forefront of this wave, providing decentralized solutions that bypass legacy systems. They unlock productivity gains and the economic growth that governments so desperately need.

Before diving into the forecasting, let’s take a step back and recap where we stand on both fronts—because understanding these forces is key to navigating what’s coming next in digital assets.

1. Debasement of Currency

Global Liquidity Update

My three-pronged, back-tested macro state indicator—which regular readers know well—has been my go-to for filtering risk-on and risk-off regimes for Bitcoin and the broader crypto market. All three components—global money supply, central bank balance sheets and the dollar—turned bullish in August, setting the stage for favourable conditions across risk assets, particularly Bitcoin and crypto.

With the business cycle bottoming out, conditions are ripe for a significant rally. Indeed, Raoul and Julian discuss this every month in their macro updates. In their latest, they address concerns about lofty valuations in equities:

“Gains driven purely by multiple expansion—rising prices without earnings growth—are sustainable as long as earnings eventually improve. Remember, prices follow the liquidity cycle, and earnings track the business cycle. Valuations seem high today because we’re still waiting for the business cycle (ISM) to turn higher.”

As the ISM index reaches its bottom and the global money supply continues to surge— largely driven by a significant decline in the dollar—Bitcoin has yet to respond. However, it’s only a matter of time before it does.

Right now, Bitcoin is like a coiled spring, ready to explode. It’s rare to see BTC trading in such a tight range mid-cycle, especially around the previous cycle’s high. Normally, these levels get blown past. I’ve discussed this a lot, and I think it’s due to the Q1 derivativesled rally hangover. Extreme positioning leading up to ETF launches caused a leverage buildup that’s taken time to unwind.

Spot buyers have been navigating this alongside Mt. Gox distributions and the German state of Saxony’s BTC sales. But with so much volume now trading at these levels, a solid support base is forming. Later in the report, we’ll dig into Bitcoin’s projections for this cycle, but I’m confident that the volume of coins changing hands here will serve as a strong support level—especially for the next crypto winter.

2. Blockchain Adoption

Now, let’s turn to “crypto,” which I’ve always defined as its own distinct category from Bitcoin. The outlook here is promising. 2024 has already been a banner year for blockchain and Web3 adoption. How do I know?

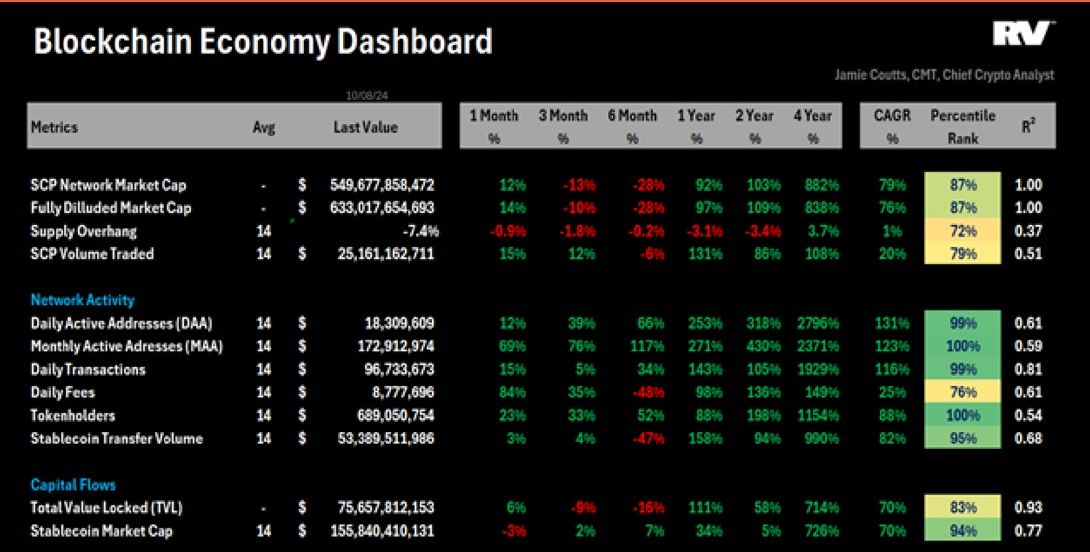

Below is the Blockchain Economy Dashboard—to my knowledge, one of the few tools that offers a comprehensive overview of the crypto ecosystem. I built it because, without a reliable way to track the fundamentals that drive network growth, everything else is just noise.

It took months to pull together, but the data here gives Real Vision Pro Crypto members some of the best-informed insights available on digital assets. Not only can you track the growing footprint of the blockchain economy, but I’ve also regressed each metric to reveal which network growth KPIs are most correlated with price. In other words, you can see which metrics carry the strongest signal for the total market cap of the Smart Contract Platform (SCP) sector.

The data doesn’t lie.

Despite total market cap sitting 28% below all-time highs, key network metrics like active addresses, transactions, stablecoin transfers, and token holders are in the 95th percentile or higher. Network activity is accelerating as we emerge from the mid-cycle correction. Just look at the one-year growth numbers:

- Daily Active Addresses (DAAs): +253%

- Transactions: +143%

- Fees: +98%

- Stablecoin Transfers: +158%

- Total Value Locked (TVL): +111%

Most network health metrics are growing at a 100% annual rate, correlating with a 79% annual growth in the SCP market cap since the birth of Ethereum in 2015. This encompasses several bull and bear markets. It’s compelling data. We always talk about secular trends, but here’s the evidence right before us. It’s not just a narrative — we’re investing beyond the narrative and building conviction in the secular trend of blockchain adoption.

Take a look at the final column in the dashboard, which is the r-squared value. It shows how much of the daily variation in the aggregate SCP market cap can be explained by changes in these on-chain metrics. At the individual asset level, these relationships can vary significantly. Some assets show very low correlation with metrics like active addresses or fees, often due to specific factors like supply overhang, vesting schedules, or even gaming of the metrics (yeah, I’m talking about the “fuckery” that goes on at the protocol level). Solana’s ecosystem might well be the worst offender, but it happens on nearly every chain.

The key takeaway is that once we aggregate these metrics for the entire sector, the shenanigans, while annoying, become less impactful. The signal becomes clear: as network metrics go up, they have a measurable impact on the sector’s market cap.

Active Addresses Indicate Prices Are Undervalued

In the next report, we’ll dive deeper into these on-chain metrics and use modelling to project the SCP sector’s valuation based on their statistical relationships. For now, the chart below, which tracks the 14-day average of Daily Active Addresses (DAAs) against the total market cap, suggests that valuations need to catch up.

DAAs are hitting new all-time highs, but prices are lagging. We saw a similar pattern in mid-2020 when DAAs first crossed 400,000. At that time, the total SCP market cap was just $42 billion —75% below the previous peak. Over the next 12 months, the market exploded to $980 billion.

While I don’t expect another 20x increase in market cap like we saw back then, the key takeaway is that the market eventually caught up to, and even overshot, the fundamentals. That rally was largely driven by massive liquidity injections from central banks and governments in the post-COVID recovery. History may not repeat exactly, but it often rhymes.

Modelling The Bitcoin Cycle Peak

In this section, I’ll walk you through the process I used to arrive at my best estimates for the bull cycle’s next (and likely final) phase. While developing these forecasts, one of my favorite quotes kept coming to mind:

The goal is not to predict the future precisely but to demonstrate a sound, data-driven approach to forecasting — one that is defensible.

Bitcoin is the benchmark for the crypto market. As I mentioned earlier, I view BTC as a distinct asset class from the rest of crypto. However, the correlation between Bitcoin and the broader crypto market is undeniable. While this relationship may evolve over time, the crypto ecosystem currently hinges on Bitcoin’s movements. That’s why modelling the cycle primarily revolves around Bitcoin.

Bitcoin is a macro asset. Though it was conceptualized decades before the Global Financial Crisis, it was born in its aftermath. It was designed to enable a new financial system, protect individual sovereignty, and counter the ongoing trend of government centralization and censorship.

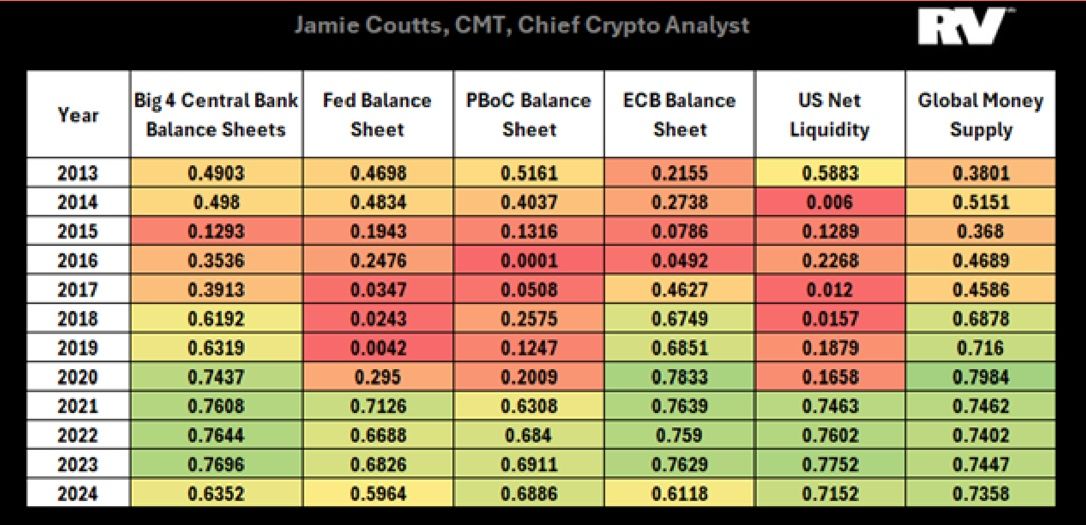

This macro element is central to the entire thesis. We know that liquidity drives asset prices. Therefore, I’ve analyzed several liquidity drivers and regressed them against Bitcoin’s price to identify the most robust relationships.

The table below shows the end-of-year R² values from a linear regression of these liquidity measures. Unsurprisingly, Global Money Supply (GLM2), which aggregates data from the world’s top 12 economies, has the strongest and most consistent correlation with Bitcoin’s price over time.

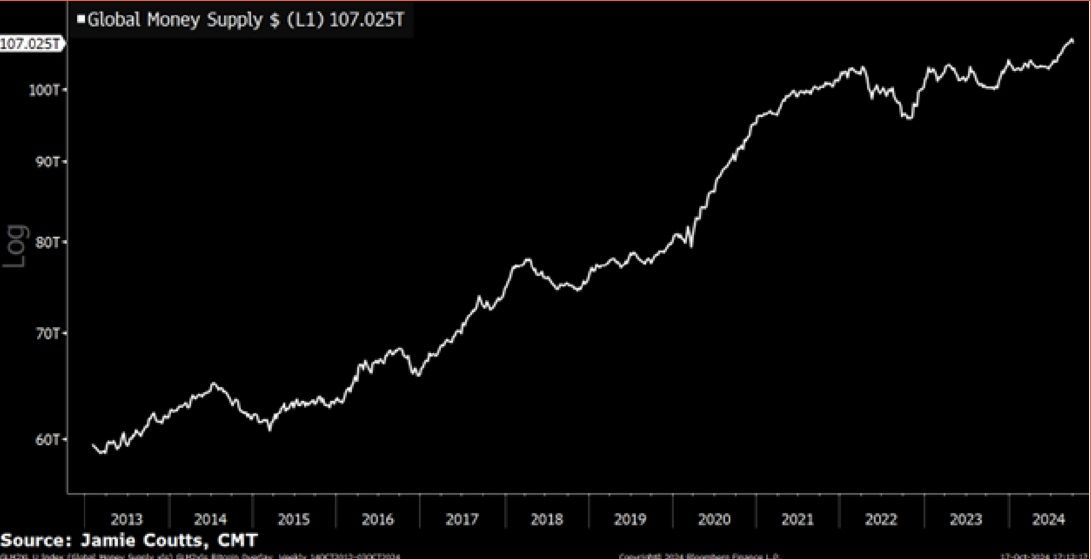

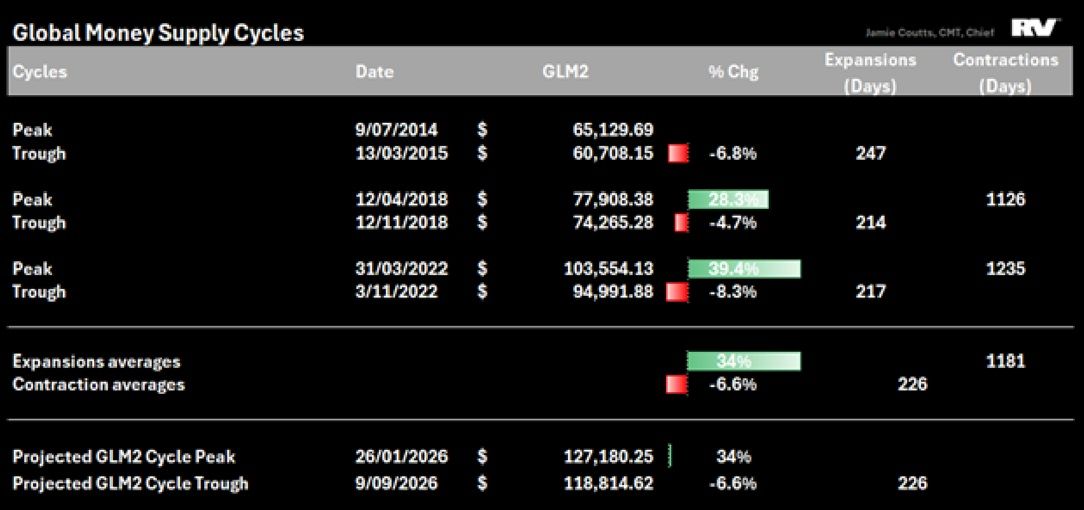

Global Money Supply (GLM2) Cycles

Today, in this the modern era of central banking — something I have termed “The Great Debasement” — the global monetary base has doubled, surging from $50 trillion in 2011 to $107 trillion by October 2024. That’s an average increase of 5.69% per year. In contrast, Bitcoin has skyrocketed from just $0.52 to $67,000 in the same timeframe, marking an astounding 133% annual growth rate. Of course, this growth has slowed in the past 5 years to just over 50% per annum.

It’s no surprise that expanding the monetary base puts upward pressure on asset prices and erodes the purchasing power of fiat currencies. At this point, the liquidity meme has become ingrained in the minds of millions, creating a self-reinforcing cycle. As more fiat money floods the economy, more capital is funnelled into anti-debasement assets like Bitcoin. With increasing demand for Bitcoin and its capped supply, the price is bound to rise.

That’s why tracking the creation and destruction of base money — the liquidity cycle — is crucial. Understanding these cycles gives us insight into when new capital will likely enter the market and push higher asset prices.

With the global money supply (GLM2) back in expansion mode, the burning questions are: when will this cycle of monetary expansion end, and how much further will the monetary base grow before that happens?

In the previous two monetary cycles during Bitcoin’s existence, GLM2 expansions lasted an average of 1,181 days, and the monetary base grew between 28.3% and 39.4% (average 34%).

Contractions, by contrast, were shorter — averaging 226 days and declining by 6.6%. This skew towards longer expansions is crucial. It’s a key insight Raoul has revealed in his exploration of “The Everything Code.”

Simply put, global central banks and governments are trapped — they cannot manage the current debt levels without monetizing it and debasing their currencies.

In a credit-based fiat monetary system, debasement isn’t a bug, it’s a feature.

Global Money Supply to Peak in Q1 2026

Extrapolating from current trends, GLM2 is projected to peak around January 2026, with a monetary base north of $127 trillion. What will likely follow is another contraction in the money supply, which, if it follows previous cycles, would infer a GLM2 of approximately $118 trillion at the back end of 2026.

This forecast employs straightforward averages of previous cycles and linear extrapolations — no fancy footwork here.

To read Jamie’s full report, sign up for Real Vision Pro Crypto using code BTC15 for your exclusive BTC Markets discount.

Feedback

If you have any feedback on Jamie's newsletter or want to request specific content, please submit a support ticket and we will respond shortly.

Disclaimer: The information provided on this page is issued by BTC Markets Pty Ltd (BTC Markets, we, us, our). The information is general only and is not intended to constitute an opinion or recommendation with respect to its contents. Past performance is not a reliable indicator of future performance. Any reference to past performance is intended to be for general illustrative purposes only. The information cannot be relied upon for any purposes and is not intended to be a substitute for professional advice.

The information does not purport to be complete, accurate or contain all of the information that a person may require to make a decision. It may also contain forward looking statements, which are subject to known and unknown risks, uncertainties, and other factors. We recommend you obtain professional advice before making any decision with respect to the matters discussed in this document.To the maximum extent permitted by law, BTC Markets will have no liability for any loss or liability of any kind: (i) arising in respect of the information contained (or not contained) on this page; or (ii) arising from a person relying on any information or statement contained on this page. The information provided is only intended for recipients in Australia. This information cannot be reproduced without our prior written permission.

Get BTC Markets content delivered

Keep up to date with the latest from BTC Markets. Unsubscribe anytime.SubscribeFind out the latest crypto news