Weekly crypto wrap: 3rd October 2024

TLDR

- Reality Check: Bull Market Correction - Real Vision's Chief Crypto Analyst.

- Cryptocurrencies continue to outperform the stock market.

- Bitcoin ETFs experience major outflow amid rising Middle East tensions.

- CME launches Bitcoin Friday Futures, achieving 31K contracts on day one.

- Retail sales rose 0.7% in Australia, the fastest pace since January.

- S&P 500 and Dow hit record highs as Fed signals no imminent rate cuts.

BTC Markets announcements

Real Vision Deep Dives with Chief Crypto Analyst, Jamie Coutts.

Reality Check: Bull Market Correction.

The past six months have been tough for crypto markets, but a strong foundation is being laid beneath the surface of volatile prices and supply overhangs. Smart contract platforms (SCP) — the backbone of the digital asset ecosystem — are quietly experiencing increased adoption and capital inflows.

Despite concerns over potential political headwinds — a Harris victory or a more fiscally responsible Republican government could impact sentiment — the basis for assessing a secular technology, Blockchain, or adoption, appears to have its own momentum at this point.

Read the preview report: ‘Reality Check: Bull Market Correction.’

Ondo (ONDO) is now live on BTC Markets.

You can buy and sell the ONDO/AUD pair on our platform. Explore this latest addition to our list of supported cryptocurrencies today.

What is Ondo (Ondo)?

Ondo Finance is a platform that uses blockchain technology to make financial markets more efficient, transparent, and accessible by automating processes and reducing costs.

For more information about Ondo (ONDO), please visit our blog. Follow us on X/Twitter, LinkedIn, or Facebook for all the latest updates.

Less than two weeks till the ASX Markets Day for Charity with BTC Markets.

Join us for the ASX Refinitiv Markets Day for Charity on Tuesday, 15th October 2024. We’re honoured to support this key event alongside industry leaders like ASX, NABtrade, Macquarie Bank, and Citi.

This day is about more than trading; it's about making a significant impact. Since 1996, the ASX Refinitiv Charity Foundation has raised over $36 million for charities focused on women, children, disabilities, and medical research.

How to get involved?

It’s simple, just log in and trade on the day and BTC Markets will contribute 100% of our trading profits to these important causes. Join us in supporting Australians in need.

Read more here.

Unpacking the ATO’s latest guidance on crypto taxes for DeFi with Crypto Tax Calculator.

Our Head of Finance, Charlie Sherry, catches up with Patrick McGimpsey from Crypto Tax Calculator to talk about the latest guidance from the Australian Taxation Office (ATO) on the taxation of Decentralised Finance (DeFi).

Watch the video here.

Plus, use our exclusive discount code BTC30 to enjoy a 30% saving on all CTC plans before 31 October 2024. View more details here.

Learn: Start your crypto journey with BTC Markets' beginner's guide.

Explore the world of cryptocurrencies with BTC Markets' beginner's guide. Our Learn Section is crafted specifically for newcomers eager to understand the crypto space.

What you’ll find in our Learn Section:

- Introduction to cryptocurrencies: Explore the fascinating world of cryptocurrencies and their potential role in the future of finance.

- Getting started in crypto: Learn the basics about crypto wallets, exchanges and creating an account.

- How to buy and sell crypto: Learn how to buy, sell, and store crypto on an exchange, and secure your assets with best practices.

- How to stay safe in crypto: Stay safe in the crypto space by understanding the common scams and how to avoid them.

- Crypto tax requirements: Understanding the regulatory landscape and tax reporting requirements for crypto.

Visit our Learn Section today and start your journey towards becoming a confident and informed crypto enthusiast. With BTC Markets, the future of finance is at your fingertips.

BTC Markets x Ticker News ‘Crypto Corner’ featuring Matt Willemsen.

In this episode of Ticker News Crypto Corner, Caroline Bowler sits down with Matt Willemsen, Head of Research & Content at Collective Shift, to dive deep into the key factors driving Bitcoin’s potential performance in Q4.

They discuss how the current market cycle differs from previous ones, the ongoing debate between Solana and Ethereum, and the importance of project-specific conferences in shaping market trends.

Watch on YouTube or Ticker News.

Mobile app fiat and crypto withdrawals.

Did you know that you can now easily withdraw fiat and cryptocurrency using our latest mobile app update?

This feature allows you to effortlessly manage your withdrawals and track transfer statuses through a comprehensive history list.

The feature is live in the most recent app release. Update your mobile app from the App Store (iOS) or Google Play Store (Android). Discover more about this exciting mobile app update here.

BTC Markets in the news

Livewire Markets: The urgent need for crypto regulation in Australia.

“Australia's approach to cryptocurrency regulation stands in stark contrast to the rapid developments observed globally. With five years of advocating for crypto regulation, I believe it's time for Australia to rethink its stance and take decisive action, to properly foster investment in local projects, businesses and assets.” – Caroline Bowler, CEO of BTC Markets.

Read the full article here.

Capital Brief: 'More questions than answers'.

“It’s super broad, the ambiguity in the language if anything just creates more questions than it provides,” Bowler said, pointing out that it remains unclear which specific activities will require a licence.

Read the full article here.

State of crypto

TLDR

- Cryptocurrencies continue to outperform the stock market.

- Bitcoin ETFs experience major outflow amid rising Middle East tensions.

- CME launches Bitcoin Friday Futures, achieving 31K contracts on day one.

- Hashdex submits amended S-1 for Nasdaq Crypto Index US ETF.

- Bitwise takes a step toward XRP ETF registration.

The weekly trading stats as of Monday, September 30th at 10:00 am AEST, based on data from Tradingview in USD.

Cryptocurrencies continue to outperform the stock market.

Canaccord, an investment banking and financial services firm specialising in wealth management and capital markets brokerage, has released its quarterly report highlighting the performance of cryptocurrencies, particularly Bitcoin (BTC). The report notes that Bitcoin has outpaced the stock market this year, posting a remarkable 140% year-on-year increase, significantly outperforming both Ethereum (ETH), which gained 60%, and the S&P 500 stock index, which rose by 30%.

Historical data suggests that a Bitcoin rally may begin between now and April, following its upcoming halving event, which has historically led to substantial price increases. Although Bitcoin’s role as an inflation hedge may diminish, it currently mirrors the behaviour of other risk assets, benefiting from the recent interest rate cut by the Federal Reserve.

The report also highlights a decline in Bitcoin's correlation with risk assets compared to previous highs. Canaccord projects that supply-demand factors post-halving, combined with the growth of exchange-traded funds (ETFs), could further strengthen the market. Additionally, stablecoin supply increased by 7% in the third quarter, reflecting ongoing expansion in the digital asset space.

Buy BTC/AUD on BTC Markets.

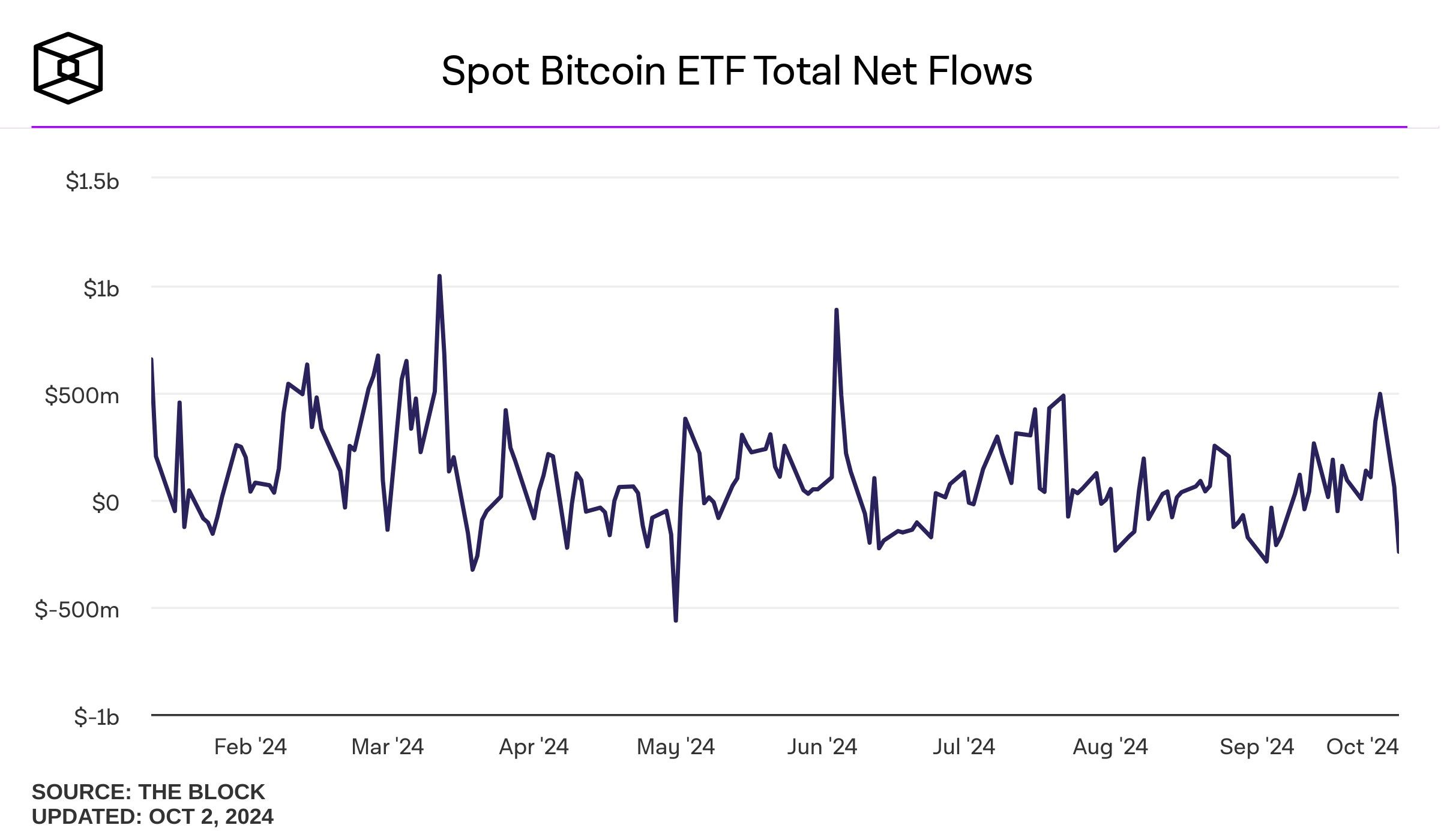

Bitcoin ETFs experience major outflow amid rising Middle East tensions.

Bitcoin ETFs experienced the largest outflow in nearly a month, totalling US$242.6 million on October 1, primarily driven by institutional investor concerns over escalating tensions in the Middle East. This shift reversed an eight-day trend of inflows, which had accumulated to US$1.4 billion.

The Fidelity Wise Origin Bitcoin Fund saw the most significant outflow at US$144.7 million, followed by the ARK 21Shares Bitcoin ETF with US$84.3 million. Other notable outflows included Bitwise (US$32.7 million), VanEck (US$15.8 million), and Grayscale (US$5.9 million). Despite these withdrawals, the BlackRock iShares Bitcoin Trust managed to record positive flows of US$40.8 million.

Source: TheBlock.co

CME launches Bitcoin Friday Futures, achieving 31K contracts on day one.

The Chicago Mercantile Exchange (CME) Group’s Bitcoin Friday Futures (BFF) launched with a record first-day trading volume, totalling over 31,498 contracts traded across two contract weeks, setting a new benchmark for crypto futures.

The new derivatives product is sized at one-50th of a Bitcoin and cash-settled every Friday against the CME CF Bitcoin Reference Rate New York Variant (BRRNY), a benchmark for BTC’s spot price.

This new product allows for short-term hedging and speculation, catering to rising demand for Bitcoin derivatives. With contracts listed every Thursday, the weekly expiry enhances liquidity and allows traders to adjust positions quickly.

Hashdex submits amended S-1 for Nasdaq Crypto Index US ETF.

Hashdex has submitted an amended S-1 filing for its proposed Nasdaq Crypto Index US ETF, indicating progress towards a potential spot cryptocurrency index ETF in the US. This filing comes as the SEC requested additional time to decide on the fund's trading authorisation. The ETF will initially include Bitcoin and Ether, the only digital assets currently in the Nasdaq Crypto US Index.

Analysts believe crypto index ETFs are the next major focus for issuers, following the successful launch of Bitcoin and Ethereum ETFs earlier this year. Franklin Templeton is also seeking to launch a similar ETF tracking the CF Institutional Digital Asset Index. As of late September, the US ETFs surpassed US$10 trillion in assets, with over US$20 billion inflows into cryptocurrency ETFs in 2024, highlighting strong interest in this investment vehicle.

Trade ETH/AUD on BTC Markets.

Bitwise takes a step toward XRP ETF registration.

Crypto native asset manager Bitwise is taking steps to create an exchange-traded fund (ETF) for XRP, the cryptocurrency linked to Ripple. The firm registered a trust entity in Delaware, marking an initial move toward filing for an ETF, like previous actions taken by companies like BlackRock and Fidelity for Bitcoin and Ethereum.

A Bitwise spokesperson confirmed the legitimacy of the filing. This announcement follows past instances where XRP ETF rumours circulated, often turning out to be false attempts to influence the token's price. Notably, a prior false filing for a BlackRock XRP ETF in November also raised speculation. Despite the news about Bitwise’s filing, XRP's price remained largely unchanged amid a broader market downturn.

Trade XRP/AUD on BTC Markets.

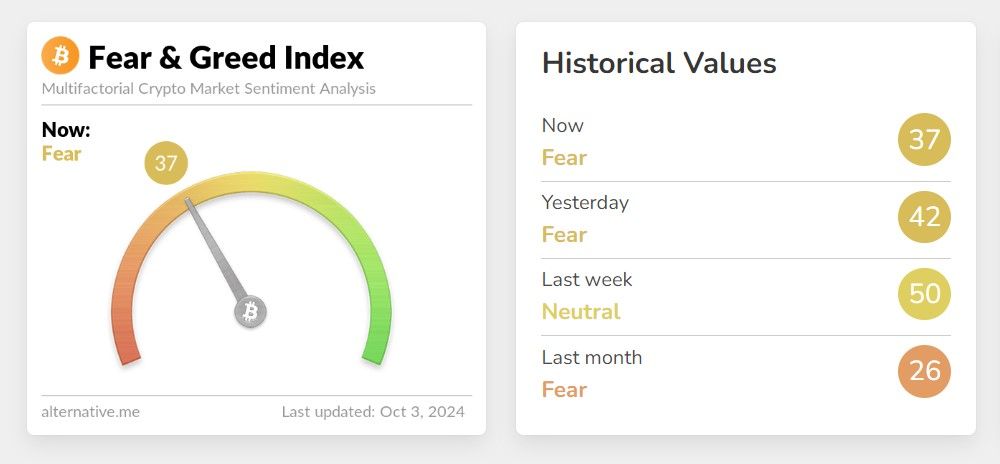

Crypto Fear & Greed Index

Source: alternative.me

The week ahead: economic events

Friday, October 4th

- United States ISM Services PMI, Non Farm Payrolls and Unemployment Rate

Saturday, October 5th

- Canada Ivey Purchasing Managers Index

Tuesday, October 8th

- Australia Business Confidence and Interest Rate

- Canada Balance of Trade

Wednesday, October 9th

- Australia Consumer Confidence MoM

- Germany Balance of Trade

Thursday, October 10th

- United States Fed Funds Interest Rate

Source: trading economics

Market reflections

Overview

In Australia, home value growth decelerated to 0.4% in September, with mixed signals in the housing market and a contraction in manufacturing. In contrast, retail sales showed modest growth. In the US, stock markets surged as the Fed maintained interest rates, supported by rising job openings and economic growth. Globally, China’s manufacturing PMI reflected uncertainty, while European inflation decreased, and Japan experienced improved consumer confidence despite steady manufacturing sentiment.

Australia

- Home value growth slowed in September, while housing credit growth also eases.

- Retail sales rose 0.7% in August, the fastest pace since January.

- Private house approvals reached a 24-month high, but dwelling approvals fall

- Manufacturing PMI dropped in September, fastest contraction since May 2020.

Home value growth slows to 0.4% in September.

Australia’s CoreLogic Home Value Index increased by 0.4% month-on-month in September, down from a 0.5% rise in July and August, indicating a slowdown in market momentum. Quarterly, housing values rose by 1%, the smallest increase since March 2023. The deceleration is attributed to more homeowners looking to sell, with new listings on the rise and weaker selling conditions reflected in auction clearance rates and private treaty sales.

Industry index shows slight improvement in September, but contraction persists.

The Ai Group Australian Industry Index rose by 4.9 points to -18.6 in September, indicating contraction for the 29th consecutive month despite modest improvements in activity, sales, inputs, new orders, and employment. The sales price indicator dropped to neutral, continuing a six-month decline, signalling increased margin pressure due to high input prices and wages. Employment contraction eased by 6.3 points to -14.3. Some sectors benefited from seasonal demand changes.

The index for the construction sector fell by 18.3 points to -19.8, showing signs of recovery despite significant delays and rising costs for permits. Increased construction enquiries were noted, but sales conversions were deferred due to high costs.

The index for the manufacturing sector dropped further into contraction, falling by 2.8 points to -33.6, the lowest level since the series began. Manufacturers faced reduced investment, increased competition, and persistent pressure from input costs and labour shortages.

Private house approvals hit 24-month high in August.

Seasonally adjusted private house approvals in Australia rose by 0.5% in August, reaching a 24-month high. This follows an upwardly revised 0.9% growth in July and marks the fifth increase this year.

Retail sales rise 0.7% in August, fastest pace since January.

Retail sales in Australia increased by 0.7% month-over-month in August, up from an upwardly revised 0.1% growth in July and surpassing market forecasts of a 0.4% rise. This marks the fifth consecutive month of growth and the fastest pace since January, driven by warm weather and Father’s Day sales events. Sales increased across all states and territories. Year-over-year, retail trade grew by 3.1%, the highest in 15 months, following a 2.4% gain in July.

Dwelling approvals drop 6.1% in August, reversing July's surge.

In August, the seasonally adjusted estimate for total dwellings approved in Australia fell by 6.1% month-over-month, reversing an 11.0% surge in July and missing market forecasts of a 4.4% decline. The drop was driven by a significant decrease in permits for private sector dwellings excluding houses, as high-density apartment approvals fell amid subdued market conditions.

Approvals for private sector houses grew at a slower pace, mainly due to a 3.9% rise in New South Wales. Geographically, total dwelling approvals declined in all other states.

Manufacturing PMI drops in September, fastest contraction since May 2020.

The Judo Bank Australia Manufacturing PMI fell to 46.7 in September from 48.5 in August, marking the eighth consecutive month of contraction and the fastest decline since May 2020. New orders and production dropped at the quickest pace in 52 months due to weakening demand, including a return to contraction in export orders. This led manufacturers to reduce purchases and inventories.

Employment declined for the fourth straight month amid low-capacity pressure. Although input and output prices continued to rise, the rate of increase slowed compared to August. Overall confidence in the manufacturing sector fell for the first time in three months, but firms remained hopeful for improved economic and geopolitical conditions in the coming year to support demand.

Housing credit growth slows to 0.4% in August.

In August, housing credit in Australia grew by 0.4% from the previous month, down from a 0.5% rise in July. Historically, housing credit in Australia has averaged 0.91% from 1976 to 2024, with a peak of 3.00% in April 1980 and a low of -0.40% in July 1984. Private sector credit increased by 0.5% month-on-month, consistent with July and market expectations. Business credit rose by 0.7%, up from 0.5% in July, while personal credit growth slowed to 0.1% from 0.5%. Annually, private sector credit grew by 5.7%, maintaining a 14-month high. The value of loans also rose by 5.7% year-on-year, matching July's pace.

Global

- S&P 500 and Dow hit record highs as Fed signals no imminent rate cuts.

- US job openings rose, inflation slowed, and the economy grew 3% in Q2 2024.

- China's manufacturing PMI shows mixed signals in September.

- Germany’s inflation hits a low, while consumer climate slightly improved.

- Japan's consumer confidence rose, while manufacturers' sentiment stayed steady.

- France's inflation dropped to 1.2%, Italy's to 0.7%, and Eurozone's to 1.8%.

United States

S&P 500 and Dow hit record highs as Fed signals no imminent rate cuts.

The S&P 500 and Dow Jones Industrial Average both reached record high closes on Monday, rebounding after Federal Reserve Chair Jerome Powell indicated that further interest rate cuts are not imminent. Powell, speaking at a business conference, mentioned the possibility of two more 50-basis point rate cuts this year, depending on economic conditions. While many investors believe the Fed’s actions for 2024 are already priced in, some, like Jake Dollarhide of Longbow Asset Management, foresee potential for more adjustments and a “soft landing” for the economy. Market expectations for a 50-basis point cut in November have slightly decreased following Powell’s remarks.

US economy grows 3% in Q2 2024, beating first quarter's revised 1.6% growth.

The US economy expanded at an annualised rate of 3% in Q2 2024, consistent with the second estimate and surpassing the revised 1.6% growth in Q1. Upward revisions were noted in private inventory investment (8.3% vs 7.5%), federal government spending (4.3% vs 3.3%), and imports (7.6% vs 7%).

However, consumer spending grew slightly less than previously estimated (2.8% vs 2.9%), with downward revisions in non-residential fixed investment (3.9% vs 4.6%) and exports (1% vs 1.6%).

The Bureau of Economic Analysis also revised GDP growth for Q1 2024 to 1.6% from 1.4%, for 2023 to 2.9% from 2.5%, and for 2022 to 2.5%, up by 0.6 percentage points.

Job openings rise to 8.04 million in August, exceeding expectations.

The number of job openings in the US increased by 329,000 to 8.040 million in August, up from an upwardly revised 7.711 million in July and surpassing market expectations of 7.655 million. Significant increases were seen in construction (+138,000) and state and local government, excluding education (+78,000), while job openings decreased in other services (-93,000).

Regionally, job openings rose in the Northeast (+65,000), South (+41,000), Midwest (+132,000), and West (+92,000). The number of hires and total separations remained steady at 5.3 million and 5.0 million, respectively. Notably, job quits fell to 3.084 million, the lowest since August 2020, down from a downwardly revised 3.243 million in July.

Core PCE price index rises 0.1% in August, signalling slowing inflation.

The US core PCE price index, the Federal Reserve’s preferred measure of underlying inflation, increased by 0.1% in August, below market expectations of a 0.2% rise and down from the 0.2% increase in July. This result aligns with the Federal Reserve’s view that inflation is slowing, supporting the case for an aggressive rate-cutting cycle. Year-over-year, core PCE prices rose by 2.7%.

US personal income grew by 0.2% in August to US$24.015 trillion, following a 0.3% rise in July and below forecasts of a 0.4% increase. Compensation of employees increased by 0.5%, driven by higher wages and salaries (0.5% vs 0.3%) and supplements to wages and salaries (0.5% vs 0.4%). However, personal income receipts on assets fell by 0.5%, with personal interest income and dividend income both declining.

Personal spending in the US rose by 0.2% in August, the smallest increase since January, following a 0.5% rise in July and slightly below forecasts of a 0.3% increase. The US$47.2 billion increase in current-dollar PCE was driven by a $54.8 billion rise in spending for services, while spending for goods decreased by $7.6 billion. The largest contributors to the increase in services were housing and financial services and insurance, while the decrease in goods was mainly due to lower spending on new motor vehicles.

Manufacturing PMI remains at 47.2 in September, indicating continued contraction.

The ISM Manufacturing PMI held steady at 47.2 in September, unchanged from August and slightly below forecasts of 47.5. This marks the sixth consecutive month of contraction in the manufacturing sector. Demand remains weak, output declined, and inputs stayed accommodative.

Timothy Fiore, Chair of the ISM Manufacturing Business Survey Committee, noted that demand remains subdued due to federal monetary policy and election uncertainty, with production stabilizing and suppliers having capacity, though shortages are reappearing.

Durable goods orders remain steady, defying pessimistic forecasts.

In August, new orders for manufactured durable goods in the US remained largely unchanged from the previous month, defying market expectations of a 2.6% drop. This stability follows a revised 9.8% surge in July, the highest in four years. The data suggests that the current slowdown in manufacturing may be temporary. Orders increased for fabricated metal products (0.6%) and machinery (0.5%), while transportation equipment orders held steady after a significant rise in July. Excluding transportation, new orders rose by 0.5%, surpassing expectations. However, orders excluding defence goods fell by 0.2%.

China

China's manufacturing PMI shows mixed signals in September.

In September, China's official NBS Manufacturing PMI rose to 49.8 from August's six-month low of 49.1, surpassing market expectations of 49.5. This marks the fifth consecutive month of contraction in factory activity, though the decline was the softest in this period. Output grew the most in five months (51.2 vs. 49.8 in August), and new orders shrank at a slower rate (49.9 vs. 48.9).

However, foreign sales fell faster (47.5 vs. 48.7), and buying levels dropped for the fifth month (47.6 vs. 47.8). Employment remained weak (48.2 vs. 48.1), and delivery times lengthened slightly (49.5 vs. 49.6). Input and output prices declined at a softer rate, while business sentiment remained unchanged.

Meanwhile, the Caixin China General Manufacturing PMI fell to 49.3 from August's 50.4, missing forecasts of 50.5 and hitting the lowest level since July 2023. New orders saw a renewed downturn, reaching their lowest in two years, and foreign sales fell the most in 13 months.

Employment shrank, and backlogs of work fell for the first time in seven months. Purchasing levels dropped amid reduced new work inflows, while output rose marginally, with growth slowing. Input prices fell the most in 15 months due to lower raw material costs, and output prices shrank at the fastest pace in six months. Business sentiment fell to its second lowest on record.

Germany

Inflation rate drops in September, lowest since February 2021.

Germany’s annual inflation rate fell to 1.6% in September, below forecasts of 1.7% and downfrom 1.9% in August, marking the lowest rate since February 2021. The cost of goods decreased by 0.3%, driven by a significant drop in energy costs (-7.6% vs -5.1%), which offset a faster rise in food prices (1.6% vs 1.5%).

Services inflation also eased to 3.8% from 3.9%. Core inflation, excluding food and energy, dropped to 2.7%, the lowest since January 2022, from 2.8%. Month-over-month, the CPI showed no growth, against expectations of a 0.1% increase. The EU-harmonised CPI fell to 1.8% annually, below the consensus of 1.9%, and decreased by 0.1% month-over-month.

Consumer climate shows slight improvement amid economic challenges.

The GfK Consumer Climate Indicator for Germany improved to -21.2 in October from -21.9 in the previous period, surpassing market expectations of -21.5. This rise was driven by increased income expectations (10.1 vs 3.5 in September) and a higher propensity to buy (-6.9 vs -10.9).

However, economic prospects declined for the second consecutive month (0.7 vs 2.0), and the tendency to save continued to rise. Despite the slight improvement, consumer expert Rolf Bürkl noted that the overall mood remains unstable due to factors like rising inflation, increasing unemployment, corporate bankruptcies, and potential job cuts.

Japan

Consumer confidence hits highest since April despite missing forecasts.

In September, Japan's consumer confidence index rose to 36.9 from 36.7 in August, though it fell short of the expected 37.1. This marks the highest consumer morale since April, with improvements in household sentiment regarding income growth, employment, and willingness to buy durable goods. However, sentiment about overall livelihood slightly declined.

Big manufacturers' sentiment holds steady at two-year high in Q3 2024.

The Bank of Japan's index for big manufacturers' sentiment remained at 13 in Q3 2024, unchanged from the previous quarter and matching market forecasts. This level is the highest in two years, reflecting a moderate economic recovery. Additionally, large firms plan to increase capital expenditure by 10.6% in the current fiscal year ending March 2025, below the consensus of 11.9%.

Eurozone

Eurozone inflation falls in September, lowest since April 2021.

The annual inflation rate in the Eurozone dropped to 1.8% in September, the lowest since April 2021, down from 2.2% in August and below forecasts of 1.9%. This brings inflation below the ECB's target of 2%.

Energy prices fell significantly (-6% vs -3%), and inflation slowed for services (4% vs 4.1%), while prices for food, alcohol, and tobacco increased slightly (2.4% vs 2.3%). Core inflation also eased to 2.7% from 2.8%.

Among the largest economies in the bloc, inflation slowed in Germany (1.8% vs 2%), France (1.5% vs 2.2%), Italy (0.8% vs 1.2%), and Spain (1.7% vs 2.4%). The ECB expects inflation to rise again later in 2024 due to the base effect of previous sharp falls in energy prices, before declining towards 2% in the second half of 2025.

France

France's inflation rate drops to 1.2% in September, lowest since July 2021.

France's annual inflation rate fell to 1.2% in September, the lowest since July 2021, down from 1.8% in August and below forecasts of 1.6%. Inflation eased for services (2.5% vs 3% in August) and remained steady for food (0.5%) and tobacco (8.7%). Energy prices dropped significantly (-3.3% vs 0.4%), as did prices for manufactured products (-0.3% vs -0.1%).

The Consumer Price Index (CPI) declined by 1.2% month-over-month, the largest drop since at least 1990, influenced by seasonal factors such as lower transport and accommodation service prices, and a decrease in energy prices. The EU-harmonised annual inflation rate also fell to 1.5%, the lowest since July 2021, down from 2.2% in August.

Italy

Italy’s inflation rate drops to 0.7% in September, lowest this year.

Italy’s annual inflation rate decreased to 0.7% in September from 1.1% in August, slightly below market expectations of 0.8%. This marks the softest increase in consumer prices since the beginning of the year.

Prices for regulated energy slowed (10% vs 14.3% in August) and non-regulated energy prices fell faster (-11% vs -8.6%), as Italy continued to secure new power supply sources following Russia’s invasion of Ukraine.

Inflation also eased for recreational and cultural services (4% vs 4.5%) and transportation services (2.5% vs 2.9%). Core inflation dropped to 1.8% from 1.9% in the previous month. The EU-harmonised inflation rate fell sharply to 0.8%, aligning with lower price growth in other major Eurozone countries, supporting expectations of potential rate cuts by the ECB.

Scam awareness

Safeguarding against cyber scams.

In today's digital world, spotting a cyber scam is more important than ever. Scams are a common way for cybercriminals to hack into accounts, putting individuals, businesses, and institutions at risk. Staying alert to scam messages is key to protecting yourself online.

Scammers use all sorts of communication methods, email, text messages, phone calls, and social media, to trick people. Their main aim is to get you to hand over money or personal information. They often pretend to be someone you trust, using that familiarity to create a false sense of security.

Read the full blog here.

The ASIC provides a checklist of common scams and ways to avoid them. To learn more, visit ASIC’s website.

Discover more on our ‘Compliance conversation’ blog page, where we share the latest updates on safeguarding against scams and protecting your assets. Stay informed and stay protected!

Want to get on our mailing list?

Sign up for free and join over 362,000 Australian traders who receive the BTC Markets Weekly Crypto Wrap.

Feedback

If you have any feedback on our newsletter or want to request specific content, please submit a support ticket and we will respond shortly.

Disclaimer: The information provided on this page is issued by BTC Markets Pty Ltd (BTC Markets, we, us, our). The information is general only and is not intended to constitute an opinion or recommendation with respect to its contents. Past performance is not a reliable indicator of future performance. Any reference to past performance is intended to be for general illustrative purposes only. The information cannot be relied upon for any purposes and is not intended to be a substitute for professional advice.

The information does not purport to be complete, accurate or contain all of the information that a person may require to make a decision. It may also contain forward looking statements, which are subject to known and unknown risks, uncertainties, and other factors. We recommend you obtain professional advice before making any decision with respect to the matters discussed in this document. To the maximum extent permitted by law, BTC Markets will have no liability for any loss or liability of any kind: (i) arising in respect of the information contained (or not contained) on this page; or (ii) arising from a person relying on any information or statement contained on this page. The information provided is only intended for recipients in Australia. This information cannot be reproduced without our prior written permission.

Get BTC Markets content delivered

Keep up to date with the latest from BTC Markets. Unsubscribe anytime.SubscribeFind out the latest crypto news