Sign up to our weekly newsletter

Stay informed on the latest market update. Subscribe to our weekly newsletter today.

Introduction

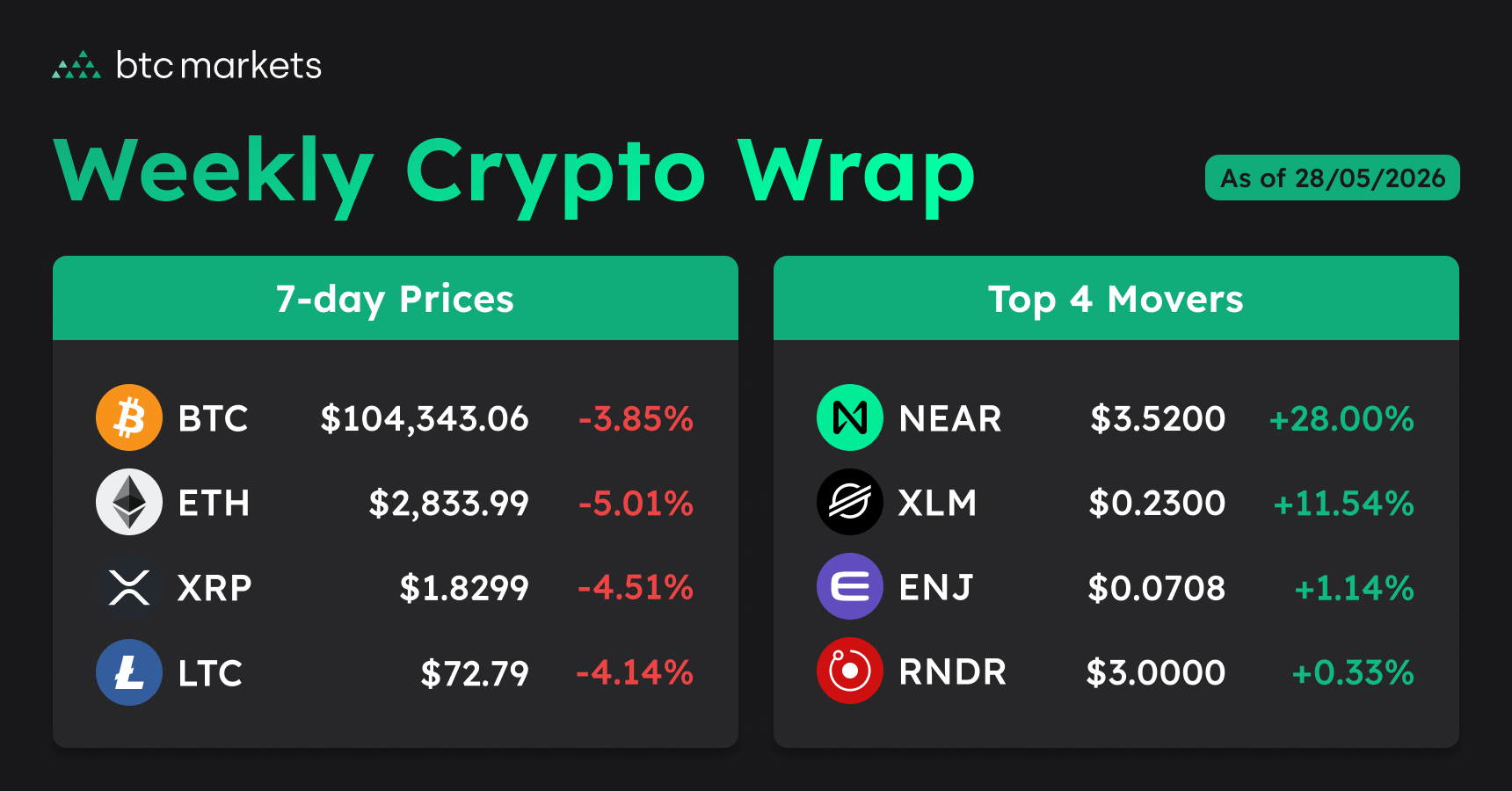

Crypto markets entered a more fragile phase this week as geopolitical tensions, ETF outflows, and oil market volatility converged across global risk assets. Bitcoin briefly fell toward US$74,260 (A$103,964) after renewed uncertainty surrounding US-Iran negotiations and the Strait of Hormuz unsettled investor sentiment heading into June. Ethereum also remained under pressure as ETF outflows extended further, while broader market positioning weakened across digital assets. Even so, institutional activity beneath the surface continued building through tokenisation projects, stablecoin infrastructure expansion, and large-scale digital asset accumulation from major firms.

Check prices on the BTC Markets exchange.

State of crypto

- Bitcoin fell toward US$74,260 (A$103,964) as geopolitical tensions intensified

- ETF outflows reached US$2.26 billion (A$3.16 billion) across two weeks

- Ethereum remained under pressure despite large institutional accumulation activity

- Hyperliquid’s HYPE token reached new highs as inflows accelerated rapidly

- Stablecoin infrastructure adoption expanded across Mastercard, SoFi, and Cash App

- The CLARITY Act advanced further through the US Senate process

Bitcoin support weakens under macro pressure

Renewed tensions involving Iran and the Strait of Hormuz became one of the market’s dominant macro drivers this week. The region handles roughly 20-25% of global oil shipments, placing energy markets firmly back at the centre of investor attention.

Risk assets broadly weakened as traders reassessed inflation expectations and liquidity conditions heading into June. Crypto markets followed equities lower, although Bitcoin continued showing relative resilience during periods of intraday volatility.

Institutional Bitcoin ETF outflows also reached approximately US$2.26 billion (A$3.16 billion) across the past two weeks, with BlackRock’s IBIT reportedly leading recent withdrawals. Markets additionally monitored reports of a US$1.29 billion (A$1.81 billion) dark pool transaction, which some analysts interpreted as broader institutional position rotation rather than outright exits from digital assets.

Technical positioning deteriorated through the week as traders focused on the US$75,800 (A$106,120) neckline tied to a potential Head and Shoulders breakdown scenario below Bitcoin’s 200-day moving average.

Check BTC

Ethereum weakness meets institutional accumulation

While Bitcoin absorbed the immediate impact of macro volatility, pressure across Ethereum markets continued building through ETF positioning and weaker short-term momentum. Ethereum continued underperforming relative to Bitcoin as spot Ethereum ETFs extended their outflow streak to eleven consecutive trading sessions. ETH traded near US$2,016 (A$2,822), while cumulative ETF withdrawals reportedly surpassed US$506 million (A$708 million).

Still, institutional positioning did not disappear quietly. BitMine Immersion Technologies announced a US$238 million (A$333 million) purchase of 111,942 ETH, reinforcing the view that larger allocators continue treating Ethereum as core digital asset infrastructure despite weaker short-term momentum. The contrast between softer market sentiment and ongoing accumulation remains one of the more notable themes across the sector.

Check ETH

Stablecoin infrastructure expansion accelerates globally

Even as spot market sentiment deteriorated, infrastructure development across traditional finance continued accelerating. Mastercard secured a New York BitLicense tied to stablecoin infrastructure following its US$1.8 billion (A$2.52 billion) BVNK acquisition. SoFi also launched SoFiUSD for more than 15 million users, while Cash App expanded USDC transfers across four blockchains for over 60 million users.

Elsewhere, DTCC confirmed plans to integrate Stellar into tokenised securities infrastructure by the first half of 2027, further signalling how major financial institutions continue preparing for blockchain-based settlement systems.

Check USDT

HYPE outperforms weakening crypto markets

Despite weaker conditions across large-cap digital assets, selective areas of the market continued attracting aggressive inflows. Hyperliquid’s HYPE token emerged as one of the strongest performers this week after reaching a new all-time high above US$64 (A$89.60).

Spot ETF inflows reportedly absorbed more than 1% of the asset’s market capitalisation within ten trading days, outpacing the relative launch pace seen across several major Bitcoin, Ethereum, and Solana ETF products.

Traders also pointed to Hyperliquid’s aggressive buyback structure and growing derivatives activity as supporting factors behind the rally, reinforcing how capital continues rotating selectively toward higher-conviction narratives.

Check XRP

Regulatory developments remain firmly in focus

Alongside shifting market positioning, regulatory developments also remained firmly in focus this week. The Digital Asset Market CLARITY Act advanced through the US Senate Banking Committee despite continued political resistance surrounding the legislation. The bill’s progress marked another meaningful step toward a clearer federal framework for digital assets in the United States.

South Korea additionally intensified enforcement efforts after prosecutors pursued the country’s first decentralised exchange rug-pull case under its new Virtual Asset Protection Act. UK authorities also sanctioned HTX under Russia-related measures, highlighting how crypto platforms are becoming increasingly exposed to broader geopolitical and regulatory pressures.

Check SOL

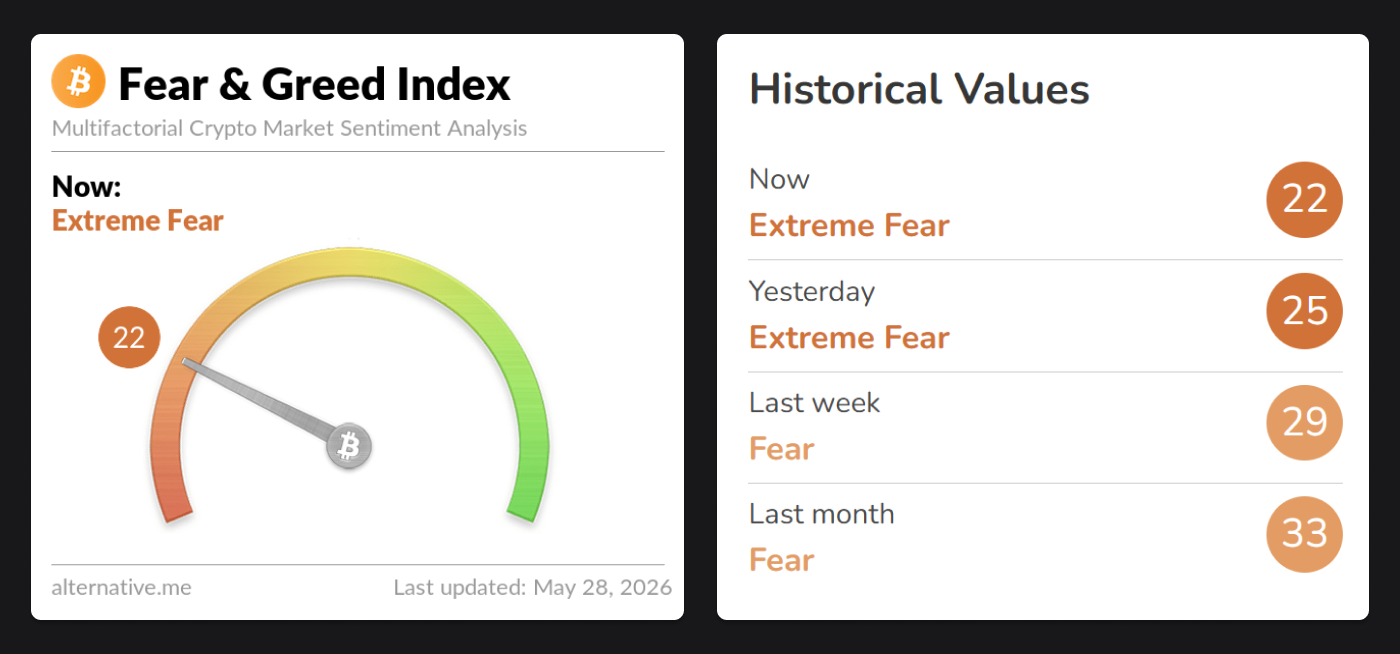

Crypto Fear & Greed Index

Source: Fear & Greed Index

Announcements

BTC Markets named finalist at the Finnies 2026

We’re proud to share that BTC Markets has been named a finalist for Best Workplace Diversity at the Finnies 2026 by FinTech Australia. Congratulations to Anastasia Varlamova, our People and Culture Manager, who is shortlisted for Emerging Fintech Leader of the Year (Under 35).

BTC Markets joins DECON 2026 as sponsor

We’re excited to support DECON 2026 and contribute to discussions on the future of digital assets in Australia. CEO Lucas Dobbins and Chief Commercial Officer Paul Stonham will join panels focused on institutional market infrastructure, capital flows and tokenised real-world assets.

The week ahead: Economic events

Thursday, May 28th

- United States Core PCE Price Index MoM, Durable Goods Orders, GDP Growth Rate, Personal Income, Personal Spending

Friday, May 29th

- Japan Consumer Confidence

- France Inflation Rate

- Italy Inflation Rate

- Germany Inflation Rate

- Canada GDP Growth Annualized, GDP Growth Rate

Sunday, May 31st

- China NBS Manufacturing PMI

Monday, June 1st

- China RatingDog Manufacturing PMI

- United States ISM Manufacturing PMI

Tuesday, June 2nd

- Euro Area Inflation Rate

- United States Job Openings

Wednesday, June 3rd

- Australia GDP Growth Rate

- United States ISM Services PMI

Source: Trading Economics

Market reflections

- United States: Inflation concerns continue weighing on household confidence

- Europe: Slowing business activity deepens pressure on the euro zone economy

- China: Beijing broadens social support measures for migrant workers

- Japan: Softer inflation data offers relief amid renewed economic uncertainty

- Australia: Labour market softening strengthens expectations of policy stability

Household sentiment in the United States weakened sharply this week as Americans grew increasingly uneasy about inflation and day-to-day affordability pressures. Higher costs across essentials such as housing, groceries and borrowing continue limiting discretionary spending confidence, while longer-term inflation expectations also moved higher. The latest data reinforced market caution around how quickly the Federal Reserve can comfortably shift away from restrictive monetary settings.

Economic conditions across Europe remained under strain after fresh business surveys pointed to a broad slowdown in private sector activity. Rising energy costs continued weighing heavily on both industrial production and consumer demand, particularly as businesses navigate weaker spending conditions and tighter margins. Investors are closely monitoring whether prolonged energy market instability could further weaken growth momentum through the second half of the year.

Policy developments in China shifted attention toward domestic support measures after authorities announced plans to improve migrant workers’ access to public services. Expanded eligibility for healthcare, education and welfare programs forms part of Beijing’s broader effort to stabilise internal consumption and reduce structural economic pressures. Markets continue assessing whether further stimulus measures may follow as policymakers balance domestic priorities against a challenging external trade environment.

In Japan, inflation slowed more than expected, easing to its weakest pace in several years. The softer reading offered some near-term relief for households and policymakers, although external cost pressures and supply-side risks continue clouding the outlook. Economists remain attentive to whether imported inflation pressures could re-emerge later this year.

Meanwhile, employment conditions in Australia showed further signs of cooling after unemployment climbed to its highest level in more than four years. The softer labour market data reduced immediate pressure on the Reserve Bank of Australia to tighten policy further, particularly as household spending and business activity remain subdued. Markets now expect policymakers to remain cautious as they assess how weaker employment conditions flow through to broader economic activity.

Consumer resilience, labour market conditions and geopolitical developments continue shaping global macro sentiment. Investors remain focused on central bank guidance and inflation expectations as policymakers attempt to balance slowing growth against lingering pricing pressures across major economies.

Final thoughts

Markets heading into June remain heavily influenced by macro conditions rather than crypto-specific narratives alone. Oil volatility, geopolitical tensions, and shifting liquidity expectations continue driving sentiment across digital assets and broader risk markets.

At the same time, institutional positioning beneath the surface continues telling a more complicated story. ETF outflows and weaker price action have not slowed stablecoin infrastructure investment, tokenisation activity, or large-scale digital asset accumulation from major firms. That disconnect between fragile sentiment and expanding institutional adoption may become one of the defining themes across crypto markets through the second half of 2026.

Ready to take advantage of the opportunities shaping the market?

Log in to trade on Australia’s own digital asset exchange and stay positioned for what comes next.

Online safety: How to stay safe from threats and extortion

Online threats can take many forms, including messages or calls that use fear or intimidation to pressure you into sharing personal details or making payments. These often appear to come from trusted sources such as government agencies, police, or financial institutions.

Some may claim you owe money, face legal action, or risk exposure of private information unless you respond immediately. The goal is to create panic and push you to act before checking if the situation is real.

What to watch out for

- Unexpected messages or calls claiming you owe money or face legal trouble.

- Pressure to make immediate payments via cryptocurrency, gift cards, or other unusual methods.

- Requests for personal, financial, or account information.

- Mentions of police, immigration, or government involvement.

- Messages that sound overly urgent, aggressive, or threatening.

How to stay safe

- End contact straight away. Hang up, delete the message, or block the sender.

- Never share personal details or make a payment without confirming the request.

- Verify any claims directly with the organisation using official contact details.

- Report the scam to authorities or Scamwatch.

- Secure your accounts immediately if you’ve shared information or made a payment.

Protect yourself and others. Learn more at scamwatch.gov.au.

Stay up to date on the latest news in the crypto space.

Sign up for free and join over 400,000 Australian traders who receive the BTC Markets Weekly Crypto Wrap.

Subscribe to our status page for live system updates or follow us on X.

Feedback

If you have any feedback on our newsletter or want to request specific content, please submit a support ticket and we will respond shortly.

Disclaimer: The information provided on this page is issued by BTC Markets Pty Ltd (BTC Markets, we, us, our). The information is general only and is not intended to constitute an opinion or recommendation with respect to its contents. Past performance is not a reliable indicator of future performance. Any reference to past performance is intended to be for general illustrative purposes only. The information cannot be relied upon for any purposes and is not intended to be a substitute for professional advice.

The information does not purport to be complete, accurate or contain all of the information that a person may require to make a decision. It may also contain forward looking statements, which are subject to known and unknown risks, uncertainties, and other factors. We recommend you obtain professional advice before making any decision with respect to the matters discussed in this document. To the maximum extent permitted by law, BTC Markets will have no liability for any loss or liability of any kind: (i) arising in respect of the information contained (or not contained) on this page; or (ii) arising from a person relying on any information or statement contained on this page. The information provided is only intended for recipients in Australia. This information cannot be reproduced without our prior written permission.

Get BTC Markets content delivered

Keep up to date with the latest from BTC Markets. Unsubscribe anytime.SubscribeFind out the latest crypto news

Crypto held its ground in a hostile week